Point Judith Lighthouse, Rhode Island

This lighthouse is known as the graveyard of the Atlantic due to high shipping traffic and dense fog along the coastline. In 1855 alone, sixteen ships were wrecked or ran aground within sight of this lighthouse.

Point Vicente Lighthouse, Rancho Palos Verdes, California

This lighthouse was constructed in 1926/ The current lighthouse stands at 67 feet tall. This lighthouse once incorporated a foghorn to warn ships during times of low visibility. The foghorn was dismantled in the early 2000s.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

UK shake-up

Early this week, the United Kingdom’s Prime Minister Keir Starmer resigned as leader of the UK Labour Party. The resignation will result in an internal leadership race within the UK Labour Party. After Starmer resigned, President Trump wasted no time in critiquing his British counterpart, stating that Starmer failed as a leader and failed the British people on immigration and energy policy.

Once the Labour Party nominates a new leader, the leader will become the United Kingdom’s sixth Prime Minister in just seven years. Quite the unstable political landscape in one of the world’s largest economies. Despite all of this political turnover, the iShares United Kingdom ETF is up 12% annualized over the last five years. We often comment on politics and its impact on markets, but for the most part, in developed economies, political leaders do not matter, as the policies enacted into law that impact markets in general are mostly moderate. We think the opportunities are in the specific bills that target niche industries, which are large tailwinds for private companies.

According to Polymarket, there is a 96% chance that Andy Burnham, a former mayor of Greater Manchester, will become the UK’s next prime minister. Unfortunately for investors, Burnham could severely pivot policy. Burham is even more left-wing than Starmer. Last fall, Burnham stated that the government should not be “in hock” to the bond market, signaling his support for even freer spending.

We are watching the race closely as it could have grave impacts on the pound, British yields, and British equities. Currently, British equities as a whole trade at a reasonable valuation. This new leadership change creates some short-term uncertainty in England which could make some investors uneasy. We also think Andy Burnham is a new risk factor which could impact British markets to come. Like always we will continue to watch especially now, as we look for non-North American developed market opportunities.

Google tumbles

Alphabet shares fell by more than 5% on Monday after John Jumper announced his departure from the firm on Friday evening. The senior research scientist is a Nobel Prize winner and is a key figure in Alphabet’s DeepMind program. DeepMind is the backbone of Google’s advanced AI models. Jumper is leaving Alphabet for Anthropic. Jumper helped create AlphaFold, DeepMind’s AI system that predicts protein structures from their amino acid sequences.

The 5% drop in Alphabet shares was its worst daily performance in over a year. The company lost $253 billion in market value on Monday alone. Alphabet shares were down almost 10% over the last month (as of 3 pm on Monday) but are still up 11% in 2026 and have more than doubled over the last year.

The departure by Jumper comes just weeks after a VP of engineering left Google for OpenAI. Wedbush’s technology analyst stated, “Losing John is a big loss for Google, and there is no way to sugarcoat it.”. The analyst went on to say that Alphabet is now losing the talent battle at the frontier of AI, and new entrants are still attracting talent as they look to go public this year. The leading companies in the industry are paying hundreds of millions to lure and attract the top talent. Alphabet’s recent stock price moves and these two major employee departures reflect compensation packages that are ultimately justified, and we expect them to potentially increase at the top of the industry.

We still like Alphabet’s valuation over the likes of OpenAI and Anthropic, but this trend of top talent leaving Alphabet is concerning for Alphabet and its investors, as progress could slow, and Alphabet could be left behind in this modern-day technology race. Alphabet also has the added benefit of a growing and strong legacy business that is producing real cash flows (and has been for quite some time). Our major concern for Alphabet and its hyperscaler counterparts is the level of spending and whether it’s sustainable. We think the large debt and equity offerings these large firms are conducting are signs that the spending is unsustainable unless something changes fast.

Before you overreact, the downtrend that Alphabet shares have faced in recent weeks has also plagued its megacap peers. Jefferies data show their trading clients have executed roughly $6 billion of net selling of Mag 7 shares in the past 20 days (as of June 22nd). That’s the second-worst 20-day stretch of selling in at least the last two years; the worst was in March of this year—close to $8 billion of net sales—in the early weeks of the Iran war.

On a positive front, it was reported on Wednesday that Alphabet was set to join the Dow and replace Verizon Communications. Analysts do not expect Alphabet shares to get a big boost after this announcement.

For now, it seems investors will continue to overreact to every news piece, which creates a volatile market environment.

Investors all in

Investors continue to pile all in on U.S. technology as investors chase returns in AI, semiconductors, and other sub-industries. According to Goldman Sachs Global Investment Research, U.S. technology funds have recorded $19.2 billion in inflows last week, the largest single weekly inflow in history. This inflow comes as SpaceX shares debuted in public markets, and President Trump announced the framework of a peace deal with Iran, where the Strait of Hormuz will be open for all vessel traffic.

Over the last four weeks, the same funds have seen $25 billion in inflows, a record for data going back to 2022. At today’s current pace, 2026 is on track for a record $154 billion in technology fund inflows, more than double the previous record set last year.

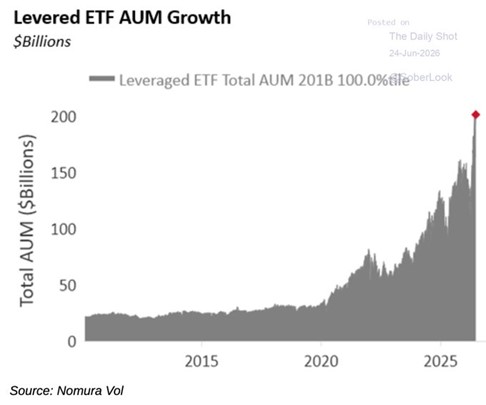

If you do not believe that everyone is all in and investors are piling their savings into growth assets, take a look at this chart below:

We are truly in the gambling stage of the market cycle where investors chase returns. Leveraged ETF assets under management have grown exponentially in recent quarters as investors ride AI and volatility to higher highs.

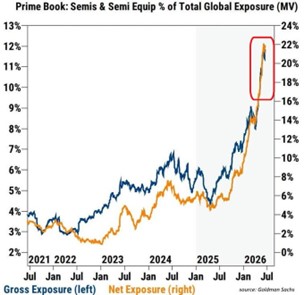

This trade is truly crowded, and it’s not just retail investors; hedge fund managers have also doubled down on the trade as they look to keep up with indices. Hedge fund long exposure to semiconductors and semiconductor equipment is at its highest point ever, with exposure more than doubling in recent months.

Hedge fund managers are now levering themselves to AI as many investors have grown impatient with the underperformance of certain hedge funds relative to indices in recent years. Hedge funds operate on very small cycles where investors criticize their quarterly returns and compare them to the performance of benchmarks and indices. Lately, indices have been roaring, and it’s mostly thanks to the AI trade as indices have been lifted heavily by the Magnificent 7, hyperscalers, and semiconductor companies. We think this is a major reason why hedge funds have piled into the crowded trade. Allocators are becoming impatient like retail traders and are all in on this trade.

Semiconductors are not the only overcrowded record trade this year. U.S. equities are on track to have record inflows this year, almost doubling the inflows seen last year (according to Bank of America Global Investment Strategy). This is further confirmation that equities as a whole are becoming crowded as investors chase returns. Historically, this happens near market tops. The crowded nature of equities has led us to alternative asset classes, including precious metals, private real estate, hedge funds, private equity, portfolio insurance, and alternative fixed income.

For our long-time readers, this is not new. For those who are new, we invest in precious metals through numerous funds in North America, including ETFs and Trusts. In terms of portfolio insurance, we operate the MacNicol Safe Harbour Fund, which invests in the Universa Black Swan Protection Protocol Fund run by Nassim Taleb and Mark Spitznagel. Through this arrangement, we expose our clients to portfolio insurance, which seeks to protect investor capital from large drawdowns in equity markets. Finally, we invest in private asset classes like hedge funds, real estate, and private equity through our Alternative Asset Trust, which launched in 2010 and has realized an annualized return of 9.8% while minimizing volatility.

The last term used two paragraphs above is new for most of our readers, as we are launching a new fund in July. The MacNicol Alternative Debt Fund (coming in July) will invest in a diversified basket of low-duration fixed-income strategies. The fund will deliver consistent income, targeting an annual yield of 6-8% with a strong emphasis on capital preservation. The strategy will focus on minimizing volatility while delivering attractive, risk-adjusted returns across market environments. MacNicol will invest directly in fixed income products and in fixed income funds. Our investment team has been doing deep due diligence on various fixed income funds across North America for numerous years and feels they have curated their list to a few high-quality managers that can navigate any type of market environment and provide strong risk-adjusted returns that reflect their respective strategies.

Disclaimer: MacNicol & Associates Asset Management invests in ETFs and mutual fund trusts that invest in physical gold, silver, and/or platinum. MacNicol & Associates Asset Management operates the MacNicol Safe Harbour Fund, which invests indirectly in strategies of Universa Investments. MacNicol & Associates Asset Management invests in private market assets through their Alternative Asset Trust, which invests in private equity, private real estate, and hedge funds.

Breakout

A long-term MAAM favorite and current holding, broke out on Tuesday by more than 10% after the company reported strong figures on its fourth-quarter fiscal year earnings after the bell on Monday. The company we are talking about is Alimentation Couche Tard Inc. (ATD). For those of you not familiar with the company, ATD is a TSX-listed company that operates convenience stores across the world.

ATD reported quarterly revenue of $19.49 billion and adjusted EBITDA of $1.59 billion (street estimates were $18.51 billion and $1.34 billion). The company reported adjusted EPS of $0.73 versus a street estimate of $0.5303 (up 56% YoY). ATD reported $5.36 billion in operating cash flow in the 2026 fiscal year, and $3.37 billion in free cash flow. The company reported strong figures across several key operating metrics, including same-store merchandise revenue growth in the U.S. and Europe. ATD also reported stronger-than-expected merchandise gross profit. The company repurchased 30 million shares during the 2026 fiscal year and reported a return on equity for Q4 of 20.2%.

The strong figures led management to increase the dividend 10.5%.

In terms of guidance, management sees organic EPS increasing by more than 10% in 2027. The company expects to open 34 new stores in the next few quarters and expects to open 750 new stores by 2030. The company also expects EBITDA improvements of $850 million by 2030. Management stated that they remain focused on maintaining a disciplined leverage profile while looking at attractive M&A opportunities moving forward.

A key takeaway from the quarterly report was EBITDA growth as the company saw increased fuel gross margins driven by commodity volatility and the company’s integrated fuel supply chain. After this earnings print, the Raymond James sell-side analyst that covers ATD stated, “This quarter highlighted the earnings power of the model in a volatile fuel environment, with outsized fuel margin capture more than offsetting softer fuel volumes,” in a note to clients. We agree with this statement and believe it is a reason ATD often outperforms in volatile periods.

ATD shares are up 21% year-to-date (as of June 23rd). We remain bullish on ATD despite the strong run shares have gone on. Shares trade at industry multiple averages in terms of P/E, P/S, and EV/EBITDA. Our thesis for ATD has not changed: consistent earnings growth driven by scale and acquisitions, paired with a defensive business mix trading at a reasonable valuation. What’s not to like from a high level? The company has also recently had a focus on capital returns to shareholders through share buybacks and dividend increases.

Disclaimer: MacNicol & Associates Asset Management holds shares of ATD across various client accounts.

Blink and you missed it

The Hang Seng Index officially entered a bear market on Tuesday, dropping 2%. The index has lost 20% since its October peak, according to Bloomberg.

The technology components of the index have led the sell-off, including Alibaba and Tencent, which are both 30% lower than their October 2025 highs:

Source: FactSet

Tencent and Alibaba account for nearly 15% of the Hang Seng Index. The Hang Seng Index comprises stocks primarily listed on the Hong Kong Stock Exchange.

The sell-off in June was caused by macro factors that reflect real weakness in the Chinese economy. Chinese retail sales contracted in May YoY for the first time since the pandemic. Chinese home prices and fixed-asset investment have also contracted in recent months. The chief economist at ING Bank stated that China’s broad economy is struggling despite pockets of strength (technology and export-related industries), which could result in policymakers having to act, in a research note last week.

The Hang Seng index also has minimal exposure to AI and its corollaries compared to other Asian indices. The AI trade has led the market this year, and this index is structurally disadvantaged when it comes to that, so it’s no surprise that it has significantly lagged other global indices.

Despite Chinese stocks as a whole and Alibaba trading at highly attractive multiples, we are still avoiding direct exposure to China. We have long liked the valuations in China but have not been able to stomach the risk associated with Chinese markets for our investors. We also believe that the economic issues in China could continue to plague markets. At the end of the day, policy uncertainty, unpredictability, weak shareholder governance, and geopolitical friction outweigh our fundamental analysis of the Chinese market. Our only exposure to China moving forward will continue to be through Emerging market ETFs. The ETF that our clients have exposure to has a 19% exposure to China (BlackRock) and 24% of its revenue (FactSet). Due to the outperformance of markets like Taiwan and South Korea, and the underperformance of China, the Chinese exposure in the ETF has decreased substantially over the last 12 months. The fund also trades at attractive multiples when compared to most developed markets.

What we are looking at next week

Markets enter the week of June 29th with investors likely increasingly focused on the market’s technical posture rather than the economic calendar itself. Major indices remain stuck near all-time highs following the post-Iran war rally. The question now becomes whether buyers have enough conviction to push this rally further or whether markets require a more pronounced period of consolidation. While economic releases including ISM manufacturing, JOLTS job openings, and the June employment report on Thursday will attract attention, investors may be paying closer attention to breadth, momentum, and leadership beneath the surface.

At the same time, precious metals have experienced a noticeable pullback following the easing of geopolitical tensions and decline in safe-haven optimism related to uncertainty around Iran. Gold and silver have both retreated from recent highs, but many investors may view the weakness as a potential buying opportunity rather than a fundamental change in trend. Central bank demand remains strong, fiscal deficits remain elevated, and the longer-term case for precious metals has not materially changed. As a result, next week may become an important test of whether recent weakness in gold and silver represents the beginning of a deeper correction or simply an oversold condition within an ongoing bull market.

Disclaimer: MacNicol & Associates Asset Management holds shares of an ETF that invests in emerging markets equities.

MacNicol & Associates Asset Management

June 26, 2026

Download in PDF format:

{kind=link}