Alappuzha Lighthouse, Alappuzha, Kerala

This lighthouse is located in the coastal town of Alappuzha, Kerala, along the Arabian Sea. It was built in 1862 to guide ships into Alappuzha’s busy port and was the first lighthouse of its kind on Kerala’s Arabian Sea coast. The tower stands 27 metres tall, features a teak spiral staircase, and remains a popular tourist attraction today.

Grand Manan, New Brunswick

This lighthouse is located on Grand Manan Island, New Brunswick, overlooking the coastline and ferry route. It was established in 1860 and remains an active lighthouse today. The original wooden tower is one of the few remaining in Canada, making it a historic and popular spot for photographers, sightseers, and wildlife viewing.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

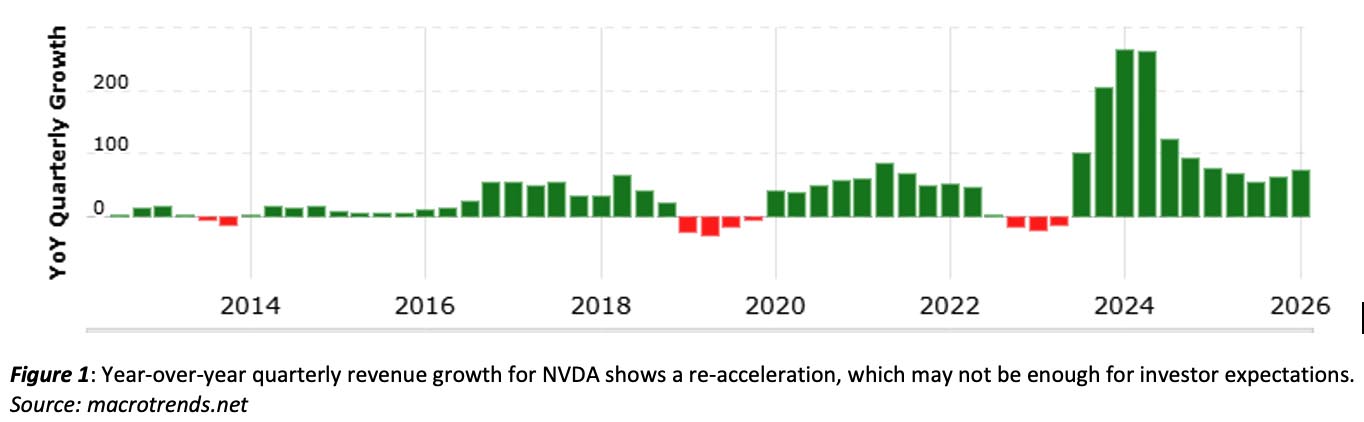

NVIDIA delivers, but investors demand perfection

NVIDIA reported earnings this week, and once again the company delivered extraordinary results. Revenue surged year-over-year, data center demand remained extremely strong, and management continued to reinforce the idea that AI infrastructure spending is still in the early innings. Yet, despite the strong quarter, the market reaction was relatively muted. The reaction says less about NVIDIA and more about where investor expectations now sit. When a company becomes the centrepiece of the AI trade, simply beating expectations is no longer enough; investors appear to be expecting nothing short of perfection.

Year-over-year quarterly revenue growth (Figure 1) has slowed down from the triple digit highs that made this the most valuable company by market cap in the world. The modest re-acceleration here appears to suggest that the AI boom is far from over, despite the market’s tame reaction to earnings.

What continues to stand out to us is that the AI story is increasingly becoming an infrastructure story rather than just a software story. Chips alone are no longer the bottleneck; power is. Data centers require enormous amounts of electricity, cooling systems, transformers, grid upgrades, and physical infrastructure. The companies enabling the expansion of power generation and electrical infrastructure may ultimately become some of the largest beneficiaries of the AI boom.

We continue to believe that AI remains a powerful long-term secular theme, but investors should recognize that the next phase of the cycle may broaden well beyond semiconductor companies alone.

Oil volatility returns

Oil prices remain volatile this week as investors continued to monitor geopolitical tensions in the Middle East alongside global supply dynamics. Markets have been struggling to determine whether recent disruptions represent a temporary geopolitical flare-up or the beginning of a more prolonged supply issue. Every headline regarding shipping routes, production risks, or diplomatic negotiations appears to move energy markets sharply in either direction, adding to the already heightened levels of investor uncertainty.

At the same time underlying demand trends remain relatively firm despite slower global economic growth. Travel demand has remained resilient, industrial activity appears to have stabilized, and emerging market consumption continues to support global energy demand.

We continue to believe energy markets could remain volatile in the coming months as geopolitical uncertainty remains elevated and collides with still-tight global supply conditions. Even if prices remain relatively range-bound in the near-term, we believe energy remains an important part of a diversified portfolio, particularly during periods of elevated global risk and persistent inflationary pressures.

The WTI is currently forming a “wedge” pattern (Figure 2) which suggests that it will likely either break out higher from here, or break down very soon. We expect any volatile move outside of the current range to likely correspond with either an escalation in tension in the Strait of Hormuz (break out higher), or a de-escalation of tension in that region (break down lower).

Disclaimer: MacNicol & Associates Asset Management holds shares of companies that are classified as oil & gas companies.

Private markets remain under the microscope

China’s dominance in rare earth metals continues despite Western efforts to ramp up domestic output. Currently, Western demand for these metals greatly outpaces Western-sourced supply. Even with heavy investment that is expected to continue, the West is at the mercy of China when it comes to rare Earth. Private markets continue to attract scrutiny following recent headlines surrounding liquidity concerns and NAV write-downs across several large funds. Investors are increasingly beginning to separate stronger managers from weaker ones, and the market is becoming more sensitive to underwriting quality, leverage, and liquidity parameters. Retail investors, specifically, are getting a lesson in what private investment actually is. As noted in a recent article by David MacNicol published in the Globe and Mail, the rush to enter this new, once-coveted investment space has left many less-informed investors scratching their heads after their first bout with a liquidity squeeze in private markets. While it has resulted in some pain, this is likely healthy for the space over the long term.

Regardless of the recent concerns, the reality is that private markets are no longer a niche corner of the market. They have become a major asset class with growing participation from both institutional and retail investors. As rates remained elevated over the last several years, many managers deployed significant amounts of capital into increasingly competitive environments. The current one is testing who is disciplined enough to not be taken in by this new wave of investment. We continue to believe attractive opportunities exist within the private space, particularly among smaller, more selective managers, but we also believe investors should remain highly focused on transparency, liquidity structures, and, ultimately, trust in management.

Gold still has a job to do

Despite gold trading near historic highs, we remain of the view that the metal has an important role to play in portfolios. Central banks across the world continue to aggressively accumulate gold reserves, geopolitical uncertainty remains elevated, sovereign debt levels continue to rise with no end in sight, and investors remain concerned about long-term currency debasement and inflation risks. Gold (and the entire precious metal space) continues to function as a form of monetary insurance during periods of uncertainty.

We also believe many investors underestimate how structurally important Central Bank demand has become for the gold market. Over the last decade global reserve managers have steadily diversified away from USD and increased exposure to gold. That trend does not appear to be slowing.

Disclaimer: MacNicol & Associates Asset Management holds shares of trust units, mutual funds, and ETFS that hold physical gold, silver, and platinum, and holds shares of companies that are classified as gold, silver, or platinum mining companies.

What we are looking at next week:

Markets enter the week of May 25th with investors continuing to focus on whether the AI-driven rally in equities can broaden beyond semiconductors and mega-cap technology stocks. NVIDIA’s earnings helped reinforce that AI demand remains exceptionally strong, but investors are increasingly shifting their attention towards second-order beneficiaries of the AI buildout, including power infrastructure and energy. Markets will also continue to monitor whether elevated valuations across the technology sector can continue to be justified as expectations remain extremely high.

Beyond AI, investors will remain focused on oil prices, geopolitical developments in the Middle East, and ongoing stress within portions of private markets. Economic data next week will include durable goods orders, consumer confidence, and PCE inflation data, all of which could influence expectations surrounding interest rates and the Federal Reserve. Gold and precious metals will also likely remain in focus as investors continue to balance strong equity market momentum against ongoing concerns surrounding debt levels, inflation, and geopolitical instability.

MacNicol & Associates Asset Management

May 21, 2026

Download in PDF format:

{kind=link}