West Quoddy Head Light, Lubec, Maine by J Hall

This lighthouse is located in eastern Maine. The lighthouse is located in Quoddy Head State Park (the easternmost point of the contiguous U.S. The original lighthouse was constructed in 1808. The current tower was built 50 years later and stands at 15 meters tall.

Garden Key Light, Florida

This lighthouse is located in the Florida Keys on Garden Key. The first lighthouse was lit in 1826. The original lighthouse and its outbuildings were originally the only structures on this key until 1846.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Private credit haircut

Early on Monday morning, while most of the eastern seaboard was commuting to work, KKR, the private asset giant, made an announcement. The asset manager announced that its largest private credit fund, managed alongside Future Standard (FS KKR Capital Corp) and held by individual investors, incurred a $560 million loss in Q1, with a growing number of loans tipping into default. The company’s NAV write-down equates to approximately 10% of the fund. This is one of the biggest indicators so far of underlying problems in a large private credit fund. Defaults in the fund jumped to 8.1% from 5.5% last quarter.

Two credit rating firms have downgraded the underlying company that operates this fund (not KKR) to junk. The fund was forced to renegotiate credit terms on loans with JPMorgan and other banks over the last few months. These renegotiated terms have made it harder for managers, including KKR, to access liquidity in their private credit funds.

As performance lags, defaults increase, and liquidity dries up, KKR announced it would be injecting $300 million into this fund. KKR will invest $150 million in preferred equity and tender for $150 million. Proceeds from this preferred share purchase will be used to support the fund’s share buyback and debt repayment. KKR also announced it will be waiving its portion of incentive fees for 4 quarters, which will support quarterly distributions in the fund.

The fund’s largest investment is reportedly underwater. Other private credit funds run by KKR for institutional investors have performed much better than this individual-focused fund. Private credit as a whole has been hit quite hard in recent quarters due to investor concerns about underwriting standards, loan quality, and concentrated exposure to software companies that are exposed to disruption from advances in AI.

KKR was not the only upper-market manager that was in the news in recent days. The Wall Street Journal reported over the weekend that Apollo is considering a # billion private credit fund. Apollo’s publicly listed BDC (a type of private credit fund), MidCap Financial Investment Corporation (MFIC), reported a quarterly loss of $61 million last week. The $3 billion fund saw defaults jump from 3.9% to 5.3% this quarter. Management has been using cash to repurchase shares in recent months due to the steep discount shares trade at. The fund trades near 85% of NAV, reflecting investors’ views on the fund and potential future losses.

Many of the investors in private credit BDCs are individuals and have the right to redeem their capital quarterly. Investors in Apollo’s private BDC asked to redeem 11% of the fund’s shares last quarter.

Looking ahead, we expect these issues to persist across the private credit landscape. However, while near-term headlines continue to dominate the narrative, the broader opportunity set is gradually improving. Many managers are not facing the large issues facing select funds due to their discipline in underwriting, moderate leverage, and lack of exposure to software companies. As we get ready to launch our alternative debt fund, we continue to monitor the sector and meet with managers of all sizes. Many smaller managers that have been extremely disciplined with their deployment of capital are not facing any headline issues.

At the end of the day, whether it’s public or private markets, we look for quality through our disciplined and stringent analysis.

We hope for all of our readers’ sake that they do not have exposure to many of the funds facing issues right now.

Chip stocks continue their hot streak

Semiconductor stocks have been on fire over the last year. Many of the headlines have been led by Nvidia, but many other companies in the space have outperformed the world’s largest company (we are not stating that these firms are better in terms of their products, revenue, or earnings, simply a comment on stock prices). This strong performance from the semiconductor industry has accelerated in recent months. Since March 30th, the iShares semiconductor ETF is up 68%, driven by strong AI infrastructure spending from companies, strong earnings and guidance, and momentum reaccelerating.

We bring this up this week because an AI chip maker, which is set to IPO, raised its offering due to strong demand. Cerebras increased its IPO offering from $3.5 billion to $4.8 billion according to filings with the SEC. This increase comes as the bull market in semiconductors is full on, with investor appetite at or near all-time highs for AI and chip stocks.

Cerebras’ chip allows for computing and memory to be fabricated on the same chip, which removes a critical bottleneck that slows things down in AI servers. This feature also puts a ceiling on memory, so the chip can only support smaller AI models. Cerebras revenue increased 76% YoY. The revenue increase was predominantly tied to 2 customers related to the UAE royal family. In 2025, 86% of the company’s sales were to the UAE. Cerebras signed a contract with OpenAI in December and added a term sheet with Amazon last month. The company’s order backlog as of December 31st was $24 billion, a large portion of which is reportedly from the OpenAI deal. Two things we do not like here are concentration (in terms of revenue exposure) and circularity. Cerebras is exposed to the circularity risk that plagues the entire AI industry, and its revenue could be gravely impacted if OpenAI misses targets and slows its spending.

We will not be buyers of the IPO for our clients as the company presents many risks that we avoid. However, researching it was very interesting and keeps us informed on the state of the sector and the underlying technology.

Rare Earth’s

China’s dominance in rare earth metals continues despite Western efforts to ramp up domestic output. Currently, Western demand for these metals greatly outpaces Western-sourced supply. Even with heavy investment that is expected to continue, the West is at the mercy of China when it comes to rare Earth metals; do not expect that to change anytime soon. BMO stated that the Trump administration has committed nearly $20 billion in funding to projects for rare earth metals so far.

China took over the industry approximately 40 years ago and currently dominates the production, processing, and refining of rare earths.

The current rare earth metals deal between the U.S. and China is still in effect, and an extension is expected to be announced, according to a U.S. official on Sunday. This statement comes as Trump and Xi are due to meet in Beijing later this week.

Rare earths are also in the news above the border. According to the Canadian government, there are 67 critical mineral projects proposed, planned, or under construction, and they’ll need a combined $72.4 billion in investment by 2034. This comes as Canada hopes to benefit from its vast resources and countries diversifying their supply chains away from China. Canada is looking for partners to make these investments. Analysts believe that Canada should utilize their rare earth metal industry as a negotiation chip with the U.S., who need Canada’s critical minerals. As of now, mining falls within the CUSMA agreements, and it is likely that those products will not be hit with tariffs.

On January 1, 2027, a new bill effectively bans Chinese rare earths in American weapon systems. This means the demand for non-China-sourced rare earths will surge as it’s mandated by law. This is where Canada hopes to swoop in.

It’s not just Canada and the U.S. that are investing heavily in rare Earths. Projects are popping up across the world as countries seek to decrease their reliance on China and companies look to capitalize on the anti-China trade.

Over the years, China’s dominance in the space has made it hard for many of these projects to get off the ground, as China has flooded the market with products, making expansion or construction of these projects unattractive. They have repeated this process over the years in order to maintain their stranglehold on the industry. Over time, China began to dominate all aspects of the industry, including technology, which set the West and others further behind. This time, it could be different as the U.S. and perhaps other countries will outright avoid China and look for alternative sources.

We continue to look for interesting opportunities in the space, but at this juncture, many of the names that are publicly listed have already gone on a massive run or are too risky for our appetite. Either way, a fascinating time for a once forgotten sector.

Speaking of China

As Trump heads to China to meet with the Chinese leadership late this week, we wanted to highlight a couple of topics that we are focused on. Beyond the Iran conflict, we expect the two sides to discuss trade policy, tariffs, cybersecurity risk, and AI, and potential steps to stabilize the relationship between the two largest economies (China and the U.S.’s relationship has become increasingly rocky in recent years, especially with Trump in the Oval Office).

This will be Trump’s first visit to China since 2017. On his 2017 trip, Trump received a $250 billion purchase commitment for U.S. products from Beijing.

Investors are hoping for a positive visit where both sides push negotiation down the road and stick to the deal negotiated last fall. The U.S. would prefer to continue to have access to Chinese rare Earth metals while they build out their supply. China would prefer to deal with someone other than Trump at a time when they have more negotiation power. Currently, China is actively looking to decrease its reliance on the West. Patience seems easy in theory, right? Unfortunately, that is not reality, and three major issues could complicate current negotiations.

Major road bumps for the two sides that will likely be discussed include Taiwan, semiconductor technology, and, of course, the closure of the Strait of Hormuz. Discussions of these topics could amplify differences between the two sides, which could negatively impact negotiations, especially with Trump leading the American delegation. According to Citibank, discussions between the two sides will likely not break the deadlock between the U.S. and Iran and expect shipping disruptions to continue in the coming weeks.

Analysts expect both sides to give in on certain issues. However, technology restrictions are likely not one that the U.S. will give ground on. The U.S. will likely receive further purchase commitments from China for products like aircraft and farm products. However, if the past repeats, China’s commitments are not always fulfilled.

We are by no means geopolitical experts, but we are paying close attention to these meetings as they could heavily impact equity and fixed income markets. We will comment further on the outcomes from Trump’s trip to China in next week’s edition of this commentary.

The bull case for gold

Over the years, we have talked about our views on gold and other precious metals. We have liked the trade for a variety of reasons over time. Despite the recent run precious metals have had, we continue to remain bullish and long on gold, other precious metals, and gold mining equities.

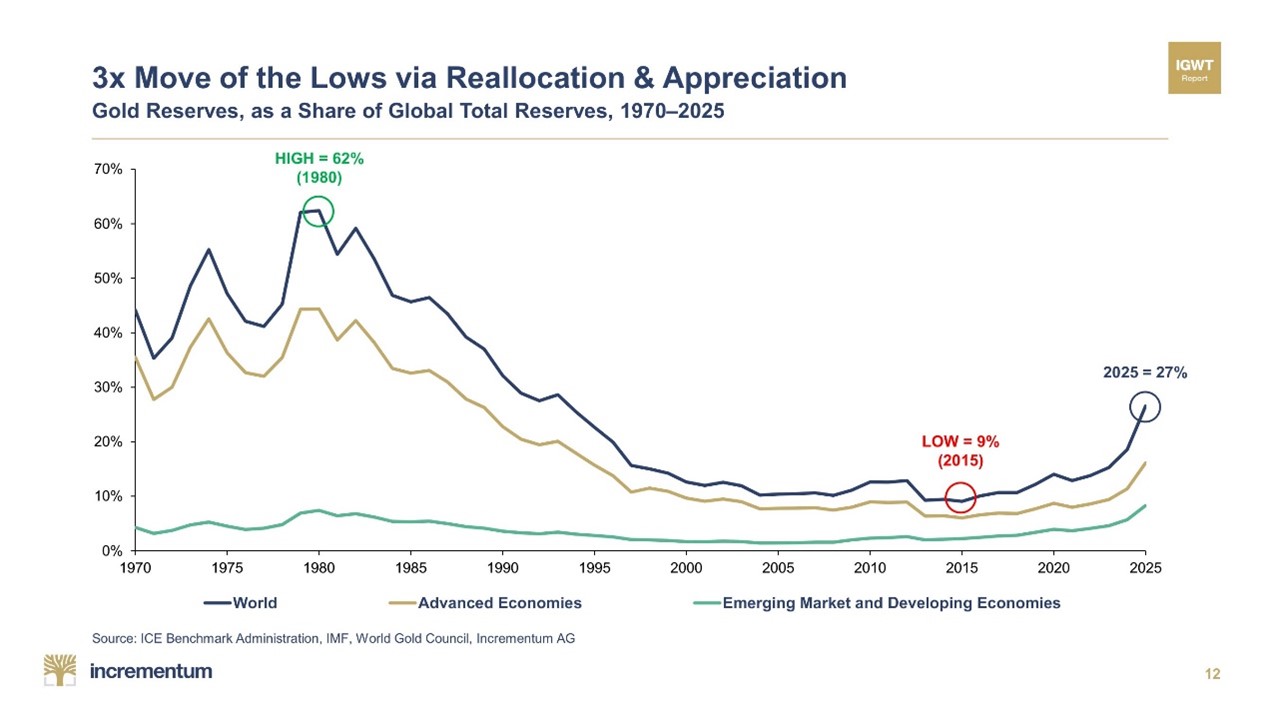

We like gold right now for a variety of reasons, including as a hedge against uncertainty and instability, as well as inflation. We also like the uncorrelated returns that it provides relative to public markets. Beyond that, we see the cyclical pivot from Central Banks across the world into gold. Central Banks have been net buyers of gold for over 15 years and continue to purchase it. In 2015, gold accounted for 9% of global reserves; today, it accounts for 27%. The 2015 share was the lowest share in the modern fiat era, according to the IMF and In Gold We Trust. Today’s share is the highest since the early 1990s and well below previous highs. Emerging markets and developing economies now hold the highest share of gold reserves in their history.

Even today, with gold near all-time highs, Central Banks continue to aggressively accumulate gold and rotate away from the U.S. dollar. This reflects a major structural change where countries are looking for monetary sovereignty, neutral collateral, and diversification.

In terms of gold mining companies, we continue to believe many are attractive at these spot levels as they continue to grow cash flows, margins, and earnings. These miners also trade at highly attractive multiples. These companies are a leveraged play on the spot price of the metal in our eyes.

Disclaimer: MacNicol & Associates Asset Management holds shares of trust units, mutual funds, and ETFS that hold physical gold, silver, and platinum, and holds shares of companies that are classified as gold, silver, or platinum mining companies.

Endowment madness

The University of Michigan’s endowment reportedly made a $20 million into OpenAI a few years ago. The investment was made before ChatGPT launched, and before Microsoft’s $1 billion investment. The school’s investment is worth more than $1 billion and is reportedly seeking a redemption amount of nearly $2 billion. Target layouts are tied to inflation, and according to documentation, early investors will be prioritized.

The University’s investment arrived in the same early cluster as investments from Reid Hoffman, Y Combinator, and Khosla Ventures.

The endowment was last valued at $21.2 billion last year. The massive return proceeds will eventually be used by a variety of sources at the school, including the athletic department.

Quite the return in a very short time for an investment vehicle with a very long-term time horizon.

We modeled our Alternative Asset Trust after the Yale Endowment Fund when we launched it in 2010. We did this for a variety of reasons, which included diversification from an investor perspective. Endowments led the charge when it came to private market assets and remain one of the largest investors in the space today.

What we are looking at next week:

Markets enter the week of May 18th with investors continuing to focus on what could possibly derail one of the strongest rallies in equities on record. The rally has been based heavily on growth and AI stocks, which have been supported by strong earnings in the last few weeks. So far even the elevated inflation numbers that we saw this week have failed to put a dent into the rally, suggesting that higher highs may be in store. The key macro events next week include Canadian CPI on Tuesday, FOMC minutes on Wednesday, and US consumer sentiment on Friday.

Technology and semiconductors will likely remain at the center of market attention ahead of NVIDIA earnings, which are due to come out after next week. AMD’s recent results helped to reinforce the narrative that AI infrastructure spending remains exceptionally strong, but next week may become more about positioning and sentiment than fundamentals alone, as the current rally is already reaching historical technical extremes. Investors will also be focused on any potential resolution to the war in the Middle East and any developments from Donald Trump’s visit to China, which are likely to dominate geopolitical discussions in the coming weeks.

MacNicol & Associates Asset Management

May 15, 2026

Download in PDF format:

The Weekly Beacon May 15 2026 US

{kind=link}