Drum Point Light, Solomons, Maryland

This lighthouse is a 47 foot tall cottage lighthouse. The lighthouse has not been active since 1962 but today it sits as a museum after being restored.

Cove Point Light, Maryland

This lighthouse was originally constructed in 1828. The lighthouse remains active today after being automated in the mid 80s. Cove Point remains an active aid to navigation and is the oldest continuously operating lighthouse on the Chesapeake Bay.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

The ramifications of large IPOs

With SpaceX and OpenAI filing paperwork over the last few weeks for potential public offerings, and AI startup Anthropic also considering going public, 2026 could be a massive year for the IPO market. The reason is that these three companies are behemoths that have grown exponentially in size and valuation in recent years. SpaceX is targeting a valuation close to $2 trillion and is looking to raise $75 billion, while OpenAI is seeking a valuation north of $1 trillion. Currently, Meta holds the record for the largest valuation when it IPO’d in U.S. history. SpaceX is seeking a valuation that is 20x Meta’s 2012 IPO valuation. Saudi Aramco is the lone historical corollary for IPOs of this size. It went public on Saudi Arabia’s stock exchange in 2019 at a valuation of $1.7 trillion.

In terms of market capitalization, these companies would rocket to the top ten in terms of companies on the Nasdaq. Two companies going public and gaining substantial market weight due to their size could be a major issue. We think this could bring heightened volatility to the market immediately. Scratch the Mag 7 or the Fantastic Five, we could see a scenario where we have the ‘Dominant 10’ that eventually accounts for more than 40% of indices.

According to Bloomberg, passive funds could have to buy up to 48% of SpaceX shares due to its size. The Nasdaq created new rules for its indices, which have been implemented this month and could trigger massive buying and selling immediately once these behemoths go public. Todd Sohn, chief ETF strategist at Strategas, told FT that SpaceX’s limited public float could make its index inclusion “frantic” as ETFs tracking trillions in assets compete for a small pool of available shares.

On top of the Nasdaq changing its rules, the Financial Times reported that the S&P Dow Jones Indices were considering rule changes that could fast-track companies into the S&P 500. This would create a new avenue of demand as both companies would become some of the index’s largest components on day one of their inclusion. This would accelerate demand for shares from passive investment vehicles, as the largest passive investment vehicles in the world track the S&P 500. On Tuesday, the FTSE Russell also announced changes to its index constitution to allow for IPO fast entry:

One thing is for sure: over the next six months, index tracking funds are going to have to buy a lot of SpaceX and OpenAI shares (if they both IPO).

These looming IPOs are massive and could be a massive transfer of wealth through share transactions from insiders and founders to passive retail investors. A successful SpaceX IPO could make Elon Musk the world’s first trillionaire. If the IPOs for these companies go well, it could cause several more companies with large valuations in private markets to also IPO.

We also think these founders are rushing to market now at all-time highs just in case (the market reverses). SpaceX and OpenAI are risky companies that have seen their valuations explode as investor sentiment and appetite have remained strong in recent years. The valuations these companies have with limited EBITDA and revenue are crazy. There is a massive demand from investors who are looking for exposure in these revolutionary high-growth companies. However, risk remains elevated, and many investors are ignoring it. These massive IPOs and extreme investor euphoria often do not occur near market bottoms; they occur when all investors are in and extremely bullish. We are not saying this is a sign of a market top with certainty, but are simply stating that it could be.

We are not the only group warning investors about these massive IPOs; Barrons published an article on Wednesday where they compared the current space craze to the 2020/2021 electric vehicle bubble. For those of you who forget, every EV startup was said to be the next Tesla, and many went belly up, leaving retail investors holding the bag. The recent space craze is not only regarding SpaceX and its valuation and eventual IPO, but numerous other space-related stocks have surged over the last 12 months.

We see similarities in this space craze with the early twenties EV bubble. Both are here to stay, but valuations of 80x sales should be a major warning sign or red flag for investors.

Oil tumbles

The price of oil tumbled on Monday despite U.S. markets being closed for Memorial Day. The price decrease followed reports of a deal between the U.S. and Iran being close. Despite Trump stating that there is no rush to get a deal done, the price of oil slid by more than 7% on Monday. According to reports, the deal would fully open the Strait of Hormuz, which would remove the major bottleneck in global energy markets. U.S. officials stated that a deal is in place but needs to be finalized by the leaders of each country.

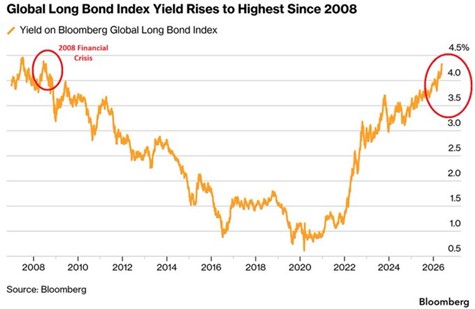

Despite Trump’s comments on there being no rush, many believe his administration is working against the clock, as this conflict has elevated energy prices across the world, which is inflationary and potentially slowed global economic growth. Trump frankly needs some wins, especially with the midterms coming. Currently, Republicans are polling quite poorly and will more than likely lose the House and potentially the Senate. Oil prices have increased by more than 70% since the start of the conflict. This price movement has spooked investors in debt markets while equities continue to run. Global yields have risen to their highest level since 2008.

We will say that it will take some time for global energy markets to return to prewar levels as production facilities must be brought back to speed. There is also a real risk that this ‘deal’ breaks down, as there have been more than five ‘deal announcements’ since the conflict began. CNBC ran a segment on Monday where they discussed each ‘deal’ announcement and how the price of oil reacted that day and in the following days. If you bought oil on every ‘deal,’ you would be up $58 despite the price of oil only increasing $25-30 during the conflict.

Not even a day later, the U.S. launched attacks on Iran, which made energy prices reverse their losses. The shift in sentiment came after the U.S. attacked two boats laying mines in the Strait of Hormuz. The IRGC warned against violations of the cease-fire and said it “considers the right to retaliate legitimate and definite,” in a statement, The Journal reported.

We think the situation is far from resolved, and energy prices will likely continue to reflect that. We hope you are not trading by following Trump’s social media account; it’s as important as ever to look through the noise.

Canadian pipelines

As global energy markets and supply chains have ground to a halt, it has become more evident than ever that Canada needs to expand and develop its energy assets to capitalize on this instability. Years of regulation and project rejections have handicapped the Canadian energy industry. We believe in the expansion and development of some of these projects and think recent events will change the minds of many Canadians, including current members of the government. We bring this all up this week, not to discuss politics, but to discuss a Canadian industry that we see a lot of value in, pipelines.

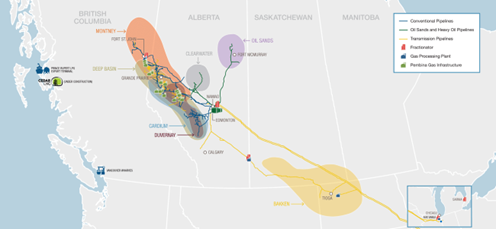

We have liked many of the names for quite some time, including Pembina Pipelines. Pembina is an Alberta-based energy transportation and midstream operator. For those of you who are unfamiliar with Pembina, here is a map of their assets from their website:

We bring Pembina up this week due to an announcement from the company on Monday. The company announced that it will be proceeding with its Heartland extraction project. The $570 million project will extract natural gas liquids. The project is expected to enter service in 2029. As part of the announcement, Pembina stated that this project will supply Dow with ethane starting in 2029. Including the Heartland agreement and the amended supply agreement, Pembina will supply Dow with a total of 57,500 bpd of ethane, a 15% increase compared to the original agreement of 50,000 bpd.

This project and the supply agreement coincide with management’s plan to continue with growth initiatives. This deal allows Pembina to monetize its liquids extraction rights on its Yellowhead land. The company expects a 5-7x EBITDA build multiple based on long-term average historical pricing and with EBITDA consisting of fixed fee revenue and frac spread exposure.

Pembina continues to strengthen its position with customers through capital-efficient growth. We like this official project announcement for Pembina as it adds to their future growth. Today, we continue to like Pembina as the company is a high-quality operator with fee-based cash flows, a strong balance sheet, and moderate growth potential. The company’s cash flows are resilient, and our investment thesis is rooted in disciplined management. We also believe Pembina remains relatively defensive, which is important in today’s environment when analyzing midstream names. The recent conflict in the Middle East has also given Canada’s energy industry a renewed strategic relevance, with Canada hopefully playing a more visible and important role in global energy flows.

Disclaimer: MacNicol & Associates Asset Management holds shares of Pembina Pipelines (PPL: NYSE) across various client accounts.

Select real estate markets heat up

As the summer weather heats up, select markets in the U.S. real estate market are also beginning to warm up. From a macro view, the housing market remains soft compared to previous times. Mortgage rates are up, transactions remain soft, and affordability remains a real issue for many potential buyers. Buyers who can are still in the driver’s seat, but their advantage is beginning to shrink, according to Redfin.

Price gains have been losing steam, according to a closely watched index. Home prices in March measured by the S&P CoreLogic Case-Shiller U.S. National Home Price Index increased 0.7% from one year prior, a slower gain than the 0.8% increase in February, according to S&P Dow Jones Indices data released Tuesday. Pending home sales, a data point that measures homes that go under contract well before the sale closes, perked up in April, rising 3.2% from the year prior, according to the National Association of Realtors. Despite some weakness in parts of the country, activity has picked up in West Palm Beach, San Jose, Chicago, and Oakland. According to luxury builder, Toll Brothers, previously lagging markets are turning around with strength in select markets in both luxury and non-luxury homes.

Redfin data points to dampened activity in recent weeks, with the recent surge in mortgage rates stemming from inflation worries and rising interest rates.

Rotation time?

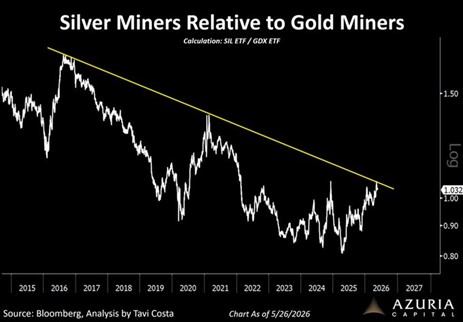

After a strong bull run for gold mining equities, it appears silver miners are on the brink of a breakout, according to technical charts.

Investors are beginning to show up as silver prices remain near $75 per ounce, while most silver miners have production costs in the $15 to $20 per ounce. These are significant margins; margins you cannot find in any other sector. Demand for silver continues to grow, which has pushed prices higher. Silver sits at the intersection of industrial demand and a financial asset. We, along with many investors, consider it a hybrid asset as it behaves like a precious metal and an industrial metal. We think spot prices will move higher, and miners typically perform like leveraged bets on the physical spot price (just like gold and gold miners last year).

We often look for numerous confirmations for our high conviction views. In our eyes, the macro backdrop is supportive of elevated silver prices moving forward, and our technical analysis also points to that.

Disclaimer: MacNicol & Associates Asset Management holds shares in mutual funds, ETFs, and equities that hold physical silver and operate in the silver mining industry.

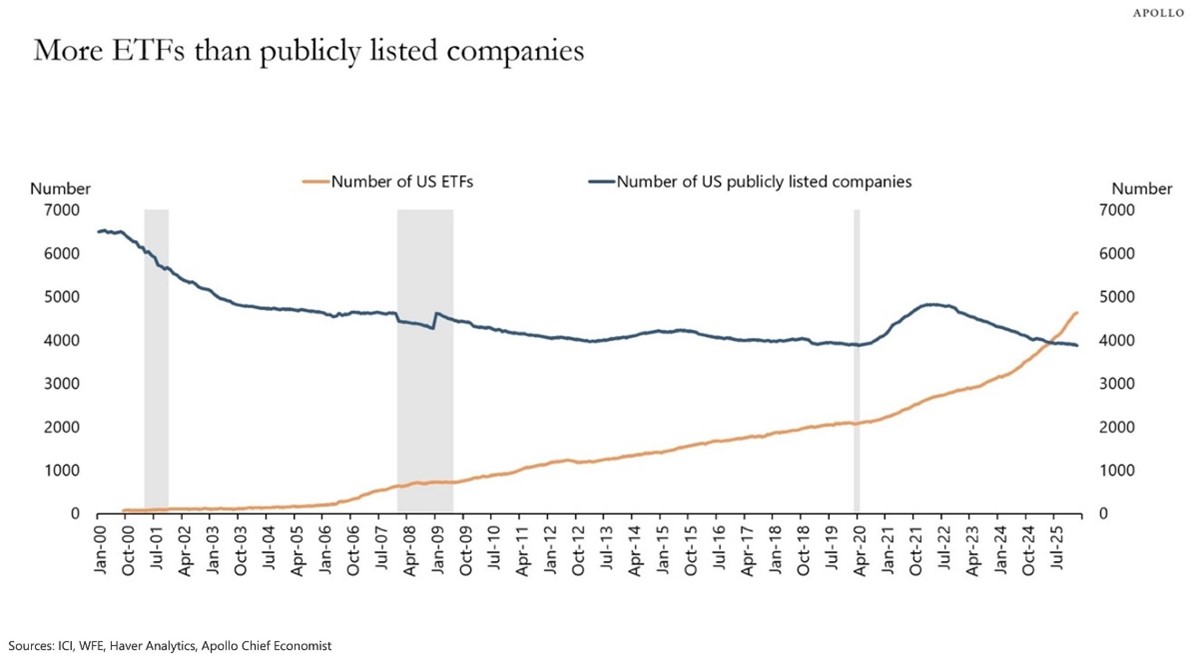

Competition in ETFs

We wanted to end this week’s edition of this publication with a really interesting chart that we ran by in a publication this week. The chart tracks the number of publicly listed companies in the U.S. and the number of active ETFs in the U.S. For the first time, there are now more ETFs in the U.S. than publicly listed companies.

Many of these ETFs hold the same companies, which is distorting the market. Investors typically pile into thematic ETFs if the sector or theme is hot. This has led to sponsors creating ETFs to match investor demand in these hot and new spaces. On top of thematic demand, retail investors are all in on buying low-cost ETFs rather than mutual funds that track broader indices. We are in a different era where investor demand has changed, and the way they invest also has.

MacNicol & Associates Asset Management

May 29, 2026

What we are looking at next week

Markets enter the week of June 1st with investors squarely focused on economic growth and labour market data following last week’s reclaiming of new all-time highs (on the S&P 500 and NASDAQ 100). The key releases next week will include ISM manufacturing on Monday, JOLTS job openings on Tuesday, and then the May US employment report on Friday, which will play a key role in determining the underlying strength of the US economy. After markets appeared to dismiss recent inflation concerns, investors will now be watching whether the economy remains resilient enough to justify current valuations and apparent continued enthusiasm around AI and technology spending.

In anticipation of what may be the largest IPO ever, the narrative next week will likely shift towards SpaceX and its trillion-dollar-plus valuation before it goes public later in June. The company is trying to position itself as an AI company with a reported $25 trillion total addressable market and to justify its valuation, especially after its prospectus showed it lost $5b in 2025. The story is obviously one of strong growth, but investors will have to decide how they see that narrative playing out over the coming months and even years. This discussion may spur investors to start considering where valuations in the broader market are, and how much longer this bull run can last.

Download in PDF format:

{kind=link}