Beachy Head Lighthouse, East Sussex, England

This lighthouse was originally constructed in 1902 below the cliffs of Beachy Head. The lighthouse stands at 33 meters tall and was originally built to replace a lighthouse at the top of the cliffs of Beachy Head.

Bull Point Lighthouse, Devon, England

This lighthouse station is located in south western England one mile north of the village of Mortehoe. The original lighthouse was built in 1879 but was subsequently replaced by a structure built in 1972. The original lighthouse was built by local merchants and landowners.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Drill baby drill

When President Trump ran for election in 2024, a big promise of his was to unlock the power of American fossil fuels. He coined this promise “drill baby drill”. His team’s reasoning for this was to reduce America’s reliance on foreign energy, reduce the power of countries in the Middle East and Russia, and strengthen a major domestic sector. A year and a half into his second term, it seems for now like this promise has come to fruition. U.S. companies are producing at record levels and investing in expanding production and upgrading energy infrastructure through major capital expenditures. This increase in supply is being driven by increased demand for U.S. energy.

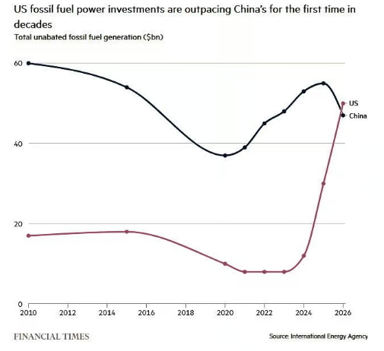

This trend has led to the U.S. outspending China on fossil fuel generation for the first time in decades.

The surge in spending by the U.S. is being driven by a surge in orders for gas-fired turbines. Most of the turbines appear to be for “behind the meter” electricity generation, where companies bypass the grid to produce their own power. A major driver of this increased demand for gas-fired turbines has been the artificial intelligence build-out as companies continue to invest in new data centers.

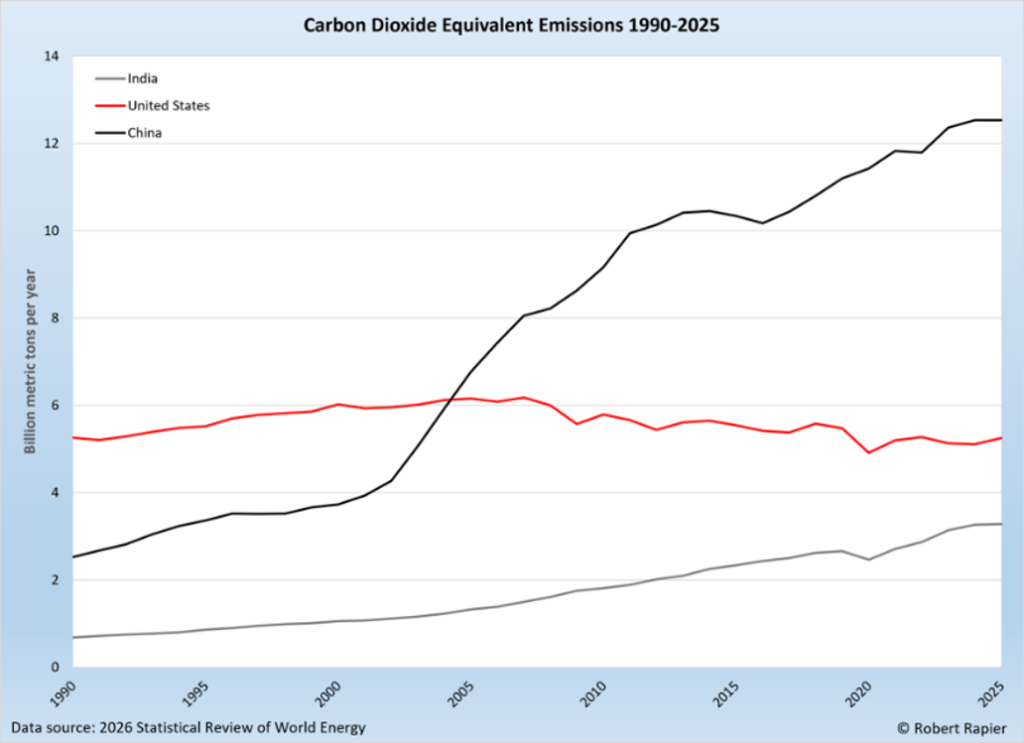

China’s investment in the area has slowed in recent years due to renewables investment and investment in coal-powered plants, which are much cheaper than gas-fired plants. Despite the Trump administration’s efforts to slow down the energy transition, the U.S. continues to expand its renewable energy capabilities. According to Ember, a think tank focused on the clean energy transition, the U.S. generated more power from solar compared to coal for the first time in May. The U.S. has vastly decreased its use of coal in recent years, cutting the energy generated from the power source in half over the last five years.

Despite China’s renewable energy leadership and heavy investment in the area, the country continues to lead the world in emissions due to its elevated reliance on coal energy and reduced regulations on fossil fuels as a whole. Do not get it twisted, energy as a whole remains much cleaner in North America and Europe.

We highlighted this topic this week as we hold several U.S. energy names. We continue to follow the top-down trends and believe many of the names that we hold in the sector will continue to benefit from the expansion of the U.S. energy sector and investment in the sector. After the last two conflicts, countries are looking to reduce their reliance on Russia and countries in the Middle East to reduce the risk of disruptions and reduce some countries’ power. European buyers continue to look to reduce their dependence on Russia, and Asian economies are looking to diversify their energy supply chains.

We think the U.S.’s next step in the energy sector should be to substantially expand the nuclear energy industry and outspend China. Nuclear power is the future and reduces emissions substantially relative to fossil fuels. It is also much more reliable than traditional renewables like solar and wind power generation. We have already seen increased investment, supportive policy, and increased demand in the industry, but we believe this needs to continue at higher rates. We think this will happen as nuclear energy continues to gain support on both sides of the aisle. Nuclear energy was once on the margins of the energy debate but has moved toward the strategic center in recent years. For investors, this shift has direct and durable implications. We think investment in the space and demand from consumers, enterprises, and governments will boost the margins, earnings, and free cash flows for producers around the world. We also believe spot uranium prices will benefit from these tailwinds down the road.

For those of you new here, we have written in depth on the topics above in previous editions of this commentary. If you are interested in our views on energy, we encourage you to look through our archives on our website.

Disclaimer: MacNicol & Associates Asset Management hold shares of U.S. energy companies, energy ETFs, and trusts that hold energy assets across various client accounts.

Insurance giant = consistent compounder

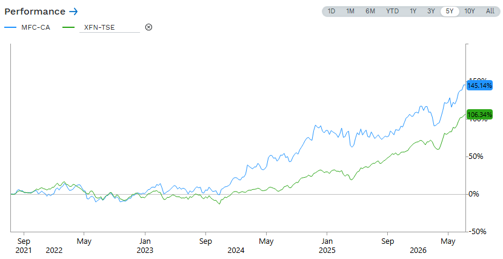

A Canadian insurance giant with global operations has quietly been one of the top large-cap companies on the TSX over the last five years. The only companies that have seen stronger performance have been Cameco, a few Canadian energy producers, and a few mining companies.

The company we are talking about is Manulife Financial, a multinational insurance company and financial services provider. The company’s stock price is up 144% over the last five years (as of July 6th). Manulife’s share price has outperformed the iShares TSX Capped Financials ETF by nearly 40% over that period:

Source: FactSet

Manulife has operations in Canada, the U.S., and Asia, with Asia serving as a long-term growth market for the company. The company’s first quarter earnings more than doubled this year to $1.1 billion, delivering EPS of $0.65. Core earnings (adjusted earnings) also increased YoY with a large increase in the company’s Asian segment. The company’s CEO said that the Asia segment achieved a 22% increase in core income and a 15% growth in new business value. The firm’s margins in its wealth management division improved YoY. Wealth management figures were boosted by a recent acquisition by Manulife. In November, Manulife completed the acquisition of private credit manager Comvest. Initially, shares pulled back on this earnings release but have since moved much higher. Shares originally pulled back as Manulife missed headline EPS estimates. Regardless of the miss, we think the company’s underlying trends remain strong, especially in its high-growth segments.

On a positive note, adjusted book value per share increased by 6% YoY. The company also decreased its financial leverage ratio to 22.5% from 23.9% the quarter before.

In the previous quarter Manulife increased its quarterly dividend by 10.2%. Currently, shares are yielding 3.3%. In February, the firm also announced that the TSX had approved its share repurchase program, under which the firm can repurchase 42 million of its common shares (2.5% of Manulife’s outstanding shares) over the next year. Since December 2023, Manulife has decreased its shares outstanding by 7.4%.

In terms of guidance, Manulife forecasts a core ROE of 18%+ by 2027.

Most recently, Manulife announced a strategic partnership in early June with Alibaba Cloud, where the companies will establish a collaborative framework to promote responsible AI innovation and accelerate the deployment of AI technology at the business level. The two firms will also explore the joint construction of an AI data center to cultivate the next generation of AI applications and develop application scenarios that align with Manulife. This collaboration will focus on solutions for the digital customer experience, specifically looking to enhance fraud detection and improve personalized services.

In terms of valuation, Manulife trades around 12.5x forward earnings, below the average for Canadian insurance providers of 14x. The firm’s return on equity is in line with industry averages, and its EPS growth is at the industry’s median level.

We write about Manulife this week after its recent performance and as we look ahead to second quarter earnings in early August. We continue to like Manulife for a variety of reasons, including the firm’s growth potential in Asia and stable North American business. We also believe management has credibility when it comes to guidance and execution while also prioritizing capital returns and strengthening its balance sheet. Finally, the firm’s valuation remains reasonable when paired with its growth and ROE profile.

Disclaimer: MacNicol & Associates Asset Management holds shares of Manulife (MFC: TSX) across various client accounts.

So much for a peace deal

Early on Wednesday morning, President Trump announced that the Iran-U.S. cease fire is over. This sent oil prices more than 5% higher, major indices lower, and VIX higher. There had been strikes from both sides leading up to this statement by Trump, which worried investors, and this announcement was the cherry on top as Trump stated that he does not want to deal with them anymore at a NATO summit and stated that negotiating with Iran was a waste of time.

Oil stocks moved much higher on Wednesday morning after a day of strong gains on Tuesday.

We told our readers and even investors on calls over the last two weeks that the probability of a prolonged conflict and higher energy prices was much higher than a complete resolution and lower energy prices. That is a major reason we have not chosen to sell our energy holdings. We think the companies we own are high-quality, cash-generating firms that will continue to see strong cash flows in the quarters to come. This conflict boosts those cash flows (for the most part).

This resurgence of strikes in the Middle East could bring significant disruptions back to the Strait of Hormuz. It also reignites inflationary fears across the world just as energy prices had pulled back substantially. We hope your portfolio is positioned to hedge some inflation over the next year. Higher energy prices will eventually bleed into the prices of other products over time.

AI companies continue to tap issuance markets

Over the last year or two, every company involved in AI has hit the debt or equity markets in order to raise capital. The companies that have done this have included private companies going public, small startups, small caps looking for growth capital, and even hyperscalers looking for capital to fuel their ambitious capex requirements. According to Dealroom, AI companies have raised $416 billion so far this year (already nearly double 2025’s figure). Even funds focused on the industry are setting records for raises. Abu Dhabi’s MGX closed a raise of $49 billion this week to back AI companies.

In May, Cerebas Systems, a semiconductor startup specializing in “wafer-scale engine” technology, IPO’d on the Nasdaq at a valuation of $95 billion and raised over $5 billion. Less than a month ago, we saw the biggest IPO ever as SpaceX raised $86 billion in an upsized offering. Although SpaceX is not a traditional AI company, it has AI ambitions that fuel its growth story. SpaceX also tapped debt markets after its IPO, raising $25 billion last month. Nvidia raised a similar amount last month in a debt issuance. Just a week before SpaceX’s IPO, we saw Google’s parent company raise over $80 billion through an equity sale to fund its AI infrastructure and compute spending. This raise by Alphabet at the time was the largest equity raise ever. Just a few months prior, Alphabet raised $30 billion in the debt market, with proceeds being used for the same purposes. This level of raising has never been seen before. Sure, new-age companies with minimal earnings tapping capital markets are normal, but mega caps like Alphabet that for a long time were buying back stock and producing positive free cash flows are not. The reason these massive firms need to raise is that they are burning capital for their AI ambitions. We simply do not think it is sustainable.

Beyond recent raises that we have seen, two of the largest private firms in the world (both AI companies – OpenAI and Anthropic) are looking to IPO in the coming quarters. Both will certainly raise substantial sums of capital to fund their spending.

We brought all this up this week due to a debt raise from Amazon. On Monday, Amazon announced it will be raising at least $25 billion in a bond sale. The firm also told its underwriters it would not be raising any more debt through this year. This debt raise comes after Amazon raised roughly $54 billion in bonds earlier this year in the U.S. and Europe, followed by a $10 billion debt issuance in Canada in June. Amazon’s borrowing spree now exceeds $100 billion since the start of 2025; Alphabet’s figure sits at nearly $90 billion, while Meta and Oracle’s figures sit in the $50 billion range. Amazon projected its cap-ex spending will reach $200 billion this year, up from $131 billion last year, with most of the spending going towards data centers, chips, and other equipment. An Amazon spokesperson told CNBC in a statement that proceeds from the latest bond sale will be used for general corporate purposes, which could include supporting investments, funding future capital expenditures and debt repayment.

According to Bloomberg data, demand settled at 1.6x the deal size. To put that number in perspective, U.S. investment-grade corporate deals have seen order demand around 4x their size so far this year. This after-demand signals the limit to the amount of money sloshing around debt markets, even for the most highly rated issuers. According to data from the raise, Amazon had to make wider concessions (a premium to where current debt trades) to price this deal.

This Amazon raise boosts this year’s total AI-linked debt sales to $335 billion (almost 2x last year’s figure). The rapid issuance has brought forth investor fatigue. We also think investors are looking for issuer diversification as equity markets are heavily concentrated in technology and the hyperscalers. Although debt and equity securities have different high-level risks, issuer risk impacts both asset classes, which could cause severe price volatility for equity and debt prices.

For now, we remain bearish on general debt markets, and any debt exposure that we have remains very short duration. All the managers and securities that we will hold in our Alternative Debt Fund (once it launches) will have short durations due to various risk factors plaguing markets and the global economy today.

What we are looking at next week:

Markets enter the week of July 13th with investors facing one of the first major tests of the second half of the year, as inflation data and the start of Q2 earnings season arrive amid a potentially volatile backdrop. June CPI on Tuesday and PPI on Wednesday will be closely watched after renewed tensions with Iran sent oil prices rising and renewed concerns that inflation could once again complicate the Fed’s path. The market has effectively been range-bound for 2 months, and the last Fed meeting resulted in a material sell-off over concerns of increased hawkishness from the new chair.

Earnings season will also begin in earnest, with the major U.S. banks reporting on Tuesday and Wednesday. Investors will be watching not only the strength of trading and investment banking revenues (especially following the SpaceX IPO) but also what bank executives say about credit conditions, loan demand, and the broader economy. With tech/growth stocks showing greater volatility recently after leading the market higher in Q2, next week could provide an early indication of whether earnings can justify elevated valuations and restore momentum, or whether leadership continues to move away from the AI/tech trade and towards other parts of the market.

MacNicol & Associates Asset Management

July 10th, 2026

Download in PDF format:

{kind=link}