Highland Light, Truro, Massachusetts

This lighthouse station was established in 1797. The current lighthouse which remains active was built in 1857. The original structure and keeper’s house remain a museum and gift shop today.

Monomoy Point Light, Monomoy Point, Massachusetts

This lighthouse was built in 1849, but the lighthouse has been inactive since 1923. The 47-foot structure has been charted as a landmark and can be visited by tourists.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Berkshire post Buffett

Over the weekend, Berkshire Hathaway announced it will acquire Arizona-based homebuilder Taylor Morrison Home. Berkshire is acquiring the company for $8.5 billion in cash, a 24% premium to its closing price on Friday. This is Berkshire’s latest push into the home-building sector and CEO Greg Abel’s biggest acquisition since taking the reins as CEO from Warren Buffett.

Taylor Morrison is the U.S.’s 6th-largest homebuilder, with developments in 12 states. The deal is expected to close at the end of this year.

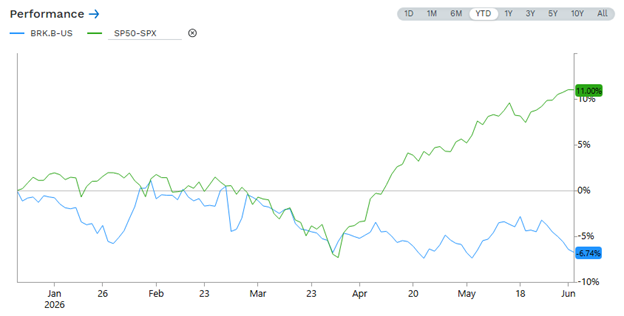

The deal signals that Abel and Berkshire are willing to make purchases with the company’s close to $400 billion cash position. Berkshire shares are down 6% year-to-date while the S&P 500 is up more than 9%.

Source: FactSet

Berkshire is likely taking advantage of weakness in the home building sector in a high-quality name. The purchase also signals confidence in the U.S. housing market, which has been struggling. Berkshire’s purchase price is paying over 1.1x the company’s book value and 9x trailing earnings. “Berkshire is acquiring a best-in-class national homebuilder, led by an exceptional team and backed by a trusted reputation for customer experience,” said Abel in the press release. Abel stated that this deal will help unify Berkshire’s homebuilding operations, which include Clayton Homes, which they acquired in 2003.

Taylor Morrison shares were up substantially on Monday morning. They have been active buyers of their own stock, which has been lagging recently. Berkshire shares moved lower on Monday due to broader market weakness.

We like this deal for Berkshire and like that Abel is beginning to find his groove. We will also warn investors that this is not huge for Berkshire, as the acquisition value is less than $10 billion and Berkshire’s market cap is more than $1 trillion.

Disclaimer: MacNicol & Associates Asset Management holds shares of Berkshire Hathaway across several client accounts.

Another one bites the dust

Just days after SpaceX and OpenAI made filings or were rumored to begin filings for their eventual IPOs, Anthropic, the U.S. artificial intelligence company that has developed Claude, filed their own paperwork to go public. This seems like a dash to the finish line as these private giants seek to raise at higher valuations and increase liquidity for investors and employees with equity. According to Barrons, Anthropic filed its S-1 with the SEC for a proposed IPO of its common stock/ No details on the raise or valuation were originally reported. Anthropic closed a funding round last week, which valued the company at $965 billion (Series H raise), topping rival OpenAI’s latest valuation of $852 billion in March.

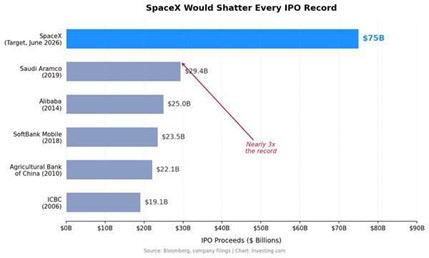

If all three of these companies IPO this year, it will likely result in the three largest raises in an IPO ever:

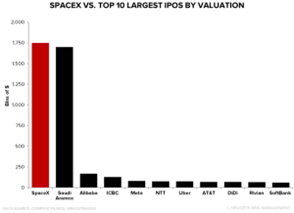

It would also result in 3 of the largest 4 valuations for AN IPO ever, as Anthropic and OpenAI are seeking valuations in the $1 trillion range and are not on the chart below:

We are truly in historic times.

Anthropic stated that the filings give it the option to go public after the SEC reviews its filings. They went on to say that market conditions and other factors would influence their eventual go-public decision.

We will state that these filings do not lock Anthropic into going public within a certain timeframe. Anthropic reported that its revenue rate exploded from $10 billion last year to $47 billion last month. Anthropic has captivated investors this year through its advanced cybersecurity capabilities. The firm has been in conversations with members of the Trump administration about its capabilities. Currently, its models are blacklisted by the Department of Defense after a clash earlier this year where negotiations broke down between the two parties. The company’s popularity grew in the private sector after this spat, as many businesses have adopted its models and AI coding tools.

Anthropic’s popularity and growth have led the firm to ink similar infrastructure deals that OpenAI has signed.

After Monday’s report that Anthropic was making its SEC filings, Zoom Video shares jumped by more than 10% due to Zoom’s $51 million investment in Anthropic in 2023. The firm made its investment through its venture arm, and its value is sitting well over $1 billion. Last month, Zoom stated that it had invested an additional $46 million in Anthropic during the first four months of this year.

So much for a peace deal

Not even a week after it was reported that the U.S. and Iran were ironing out the final details on a cease-fire and resolution to the conflict, Iran has again suspended talks. According to an Iranian source, discussions between the two were suspended after Israel carried out attacks against Lebanon.

This sent oil prices higher after some relief last week.

We warned our readers that the reports last week could be a bit optimistic and early. We ended up being right and continue to believe that energy prices will remain elevated due to the conflict in the Middle East, which we do not foresee being solved in the near future.

This week, we dove into some research and presentations from industry experts in oil and gas to get an updated picture of the state of the sector. Many experts believe the conflict in Iran will continue for some time, and it will be a prolonged low-aggression conflict similar to past wars in the Middle East. There is a major belief that Iran has an interest in prolonging the war into November until the midterm elections to show the impact of another American foreign conflict. We also think Iran and the U.S. remain extremely far apart on finalizing a deal as Iran still wants to tax cargo in the Strait of Hormuz and continue their uranium program while the U.S. is outright against that happening.

So why does that matter for energy markets? Oil prices have already spiked but are being held in place by mass strategic petroleum reserve releases (mostly from the U.S.), small spare capacity, and slight demand destruction. Bloomberg expects these SPR releases by the U.S. to only be possible for another 12-13 weeks (at the current release rate). That could lead to large price spikes by the end of the summer.

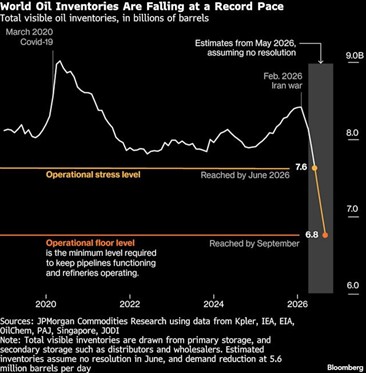

Last month, Bloomberg posted a chart of global oil inventories, which have rapidly decreased since the start of the Iran conflict and will continue to decrease as the war continues.

Bloomberg’s oil and gas analyst pointed to geopolitical conflict being the new norm and believes oil prices will reflect a risk premium moving forward, even if the Iran war ends. He believes this risk premium and securing a reliable supply will benefit the only two large democratic oil producers for years to come, Canada and the U.S.

We share similar thoughts and add to our energy exposure even before this conflict. Countries, especially those that rely on the Middle East, will look to other countries like Canada for supplies to limit disruptions moving forward. Most of Asia depends on Middle East oil, and Asia is the growth engine for demand across the world. Currently, many of the poorer countries are facing serious shortages due to the conflict and are actively looking for supply alternatives. This is where we think North American producers can benefit, specifically Canadian producers. Many of these companies are highly attractive in terms of price multiples and are producing extremely attractive cash flows, and are boosting their return to shareholders. For years, Canadian producers had one customer, the U.S., which led to them selling at a near $20 discount per barrel. That discount has decreased and is expected to continue to decrease as more countries look to Canadian energy. This discount decrease will directly lead to a margin expansion for producers, which is a highly attractive opportunity for investors, including us.

Alphabet files for huge offering

It seems private companies are not the only organizations attempting to raise money in today’s hyped up and high-growth market. On Monday at market close, Alphabet announced an $80 billion equity issuance that the firm will use to fund its AI infrastructure buildout. It was revealed later that $10 billion was raised privately from Berkshire Hathaway (quite the busy week for CEO Greg Abel).

The overall offering includes $30 billion in concurrent public offerings consisting of $15 billion in preferred stock and $15 billion in its common A and C shares. Berkshire’s investment is not included in any of those numbers and was negotiated privately at a 6% discount to current Alphabet share prices.

Shares immediately fell on the raise news, but Alphabet shares have been on fire in recent months as the technology company fully embraces AI and builds out its own platform, Gemini, which many consumers prefer due to its integration with various applications and the existing Google ecosystem.

Over the last year, Alphabet has raised over $85 billion in debt and continues to report strong (although depleting) cash flows. The company, along with other hyperscalers, continues to heavily invest in AI infrastructure. In their most recent earnings call, Alphabet stated that capital spending would total $180 to $190 billion in 2026. It also stated that 2027 spending would significantly increase relative to 2026. With these spending levels, it’s no surprise that Alphabet has tapped equity and debt markets in the last year, especially with the state of the market and investor sentiment remaining so bullish on AI. Alphabet, along with other hyperscalers, is expected to spend hundreds of billions on capex infrastructure, which many forecast will outpace operating cash flows.

Berkshire’s investment in Alphabet increases its stake in the technology company. Their total Alphabet holdings equate to more than $32 billion after this announcement, making it Berkshire’s 4th largest equity holding.

This issuance by Alphabet reflects where we are in the cycle (in our eyes). Once a large share repurchaser is now issuing equity in order to finance and expand operations. There is a reason Alphabet chose to make this filing now: management wants capital, and they do not want to wait for the market to change, which could impact investor appetite. The main issue for us is that this capital is being raised to spend on data centers that currently have negative returns on invested capital. Right now, the train keeps going; if something happens, it could come screeching to a halt and change the minds of many investors. Oppenheimer brought an interesting point of view for this raise, stating that this equity issuance is because credit is drying up.

Ultimately, the raise by Alphabet is not extreme when you look at their $4.7 trillion market cap, so dilution effects are very minimal.

We are positioned to protect our investors’ capital from the risks highlighted above without mortgaging the upside. We are not stating that something bad is looming; we are just pointing to the major risk factors in today’s market. We will also say that out of the hyperscalers, Alphabet’s business model is our favourite, and it once looked attractive from a valuation standpoint, which we noted in this publication. Today it is back to being a tad on the expensive side from our point of view, especially with the risks present in today’s market.

In our eyes, protection comes in numerous forms, including portfolio insurance, precious metals, and other assets with low correlation to underlying indices.

Hewlett-Packard again?

Over the last few weeks, we wrote about Hewlett Packard Enterprises, a company that we have talked about for a few years now in this commentary. We talked about the company’s recent outperformance. The outperformance over the last year has been driven by a rerating of the story as investors become more confident in the company’s AI story. HPE has seen surging demand for its AI servers, networking strength from its acquisition of Juniper Networks last year, strong guidance, and a valuation catch-up. We have been talking about a few of these topics for a few quarters now, but never foresaw the turnaround to be this quick and the demand to remain this robust.

This week, we are highlighting the company due to its recent earnings release, which led shares to jump more than 25% on Tuesday. As of 11 am EST on Tuesday, shares are up 147% year-to-date. The company beat FactSet revenue estimates by 9% while networking revenue jumped 148% year-over-year. On the earnings front, EPS surprised by more than 40% this quarter. Free cash flow came in at $915 million this quarter versus $847 million last year. The company also provided extremely strong guidance where EPS for fiscal year 2026 was increased to $3.35 to $3.45 from prior guidance of $2.30 to $2.50. Revenue growth was guided up for FY26 to 29-33% from 17-22% and FactSet’s estimate of 19.2%. FY26 free-cash-flow was guided to $3.5 billion from prior guidance of $2 billion. Fiscal year 2027 guidance also came in higher than expected relative to FactSet’s street estimates.

On the company’s earnings call, management stated that 75% of free cash flow will be returned to shareholders once 2x net leverage is reached (expected at the end of 2026, two years ahead of target). The company expects the full benefits of its Juniper Networks acquisition to be realized in fiscal year 2027. The company also stated that it continues to focus on the expansion of its agentic AI capabilities across storage, data protection, and its GreenLake Cloud platform.

Investor sentiment was extremely positive on this meaningful quarterly beat and guidance raise. The guidance raise was powered by strong demand and market share gains. The company continues to boast a strong order backlog. Most sell-side analysts raised their price target for HPE as the company continues to be rerated from a value technology company with moderate growth to a fast growth company benefiting from the AI transformation.

Disclaimer: MacNicol & Associates Asset Management holds shares of Hewlett Packard Enterprises (HPE) across several client accounts.

MacNicol & Associates Asset Management

June 5, 2026

What we are looking at next week

Markets enter the week of June 8th with investors focused on inflation after digesting this week’s May employment report, which comes out Friday. Estimates are for 95k jobs gained in the month, which would be generally positive and would allay any broader fears of an immediate economic slowdown. That number, along with the market reaction to it, will have a strong effect on investors going into next week. The key inflation releases next week will be the May Consumer Price Index (CPI) on Wednesday, followed by the Producer Price Index (PPI) on Thursday. After several months in which geopolitical tensions, economic growth, and corporate earnings have overshadowed inflation concerns, next week’s data will help determine whether markets can continue to look through elevated price pressures or whether interest rate expectations begin moving higher once again. We note that both CPI and PPI readings last month were multi-year highs, and if we were to get more elevated inflation numbers, investors (and the Federal Reserve) would likely no longer be able to ignore the mounting pressure.

Beyond the economic data, investors will continue assessing whether the AI-driven rally can broaden beyond a handful of mega-cap technology companies. NVIDIA’s earnings once again highlighted the extraordinary level of spending taking place across AI infrastructure, but the next phase of the story may be less about earnings and more about whether that spending ultimately translates into broader productivity gains and corporate profits. Investors will also be watching oil prices, geopolitical developments, and bond yields, all of which remain important variables for a market that has shown remarkable resilience despite a growing list of macroeconomic risks.

Download in PDF format:

{kind=link}

{kind=link}