Ploumanac’h lighthouse, Perros-Guirec, France

This lighthouse was originally constructed in 1860 but was destroyed in 1944 by German troops. It was replaced with a new structure in 1946 and stands at 15 meters tall.

Gilbert’s Cove Lighthouse, Nova Scotia

This lighthouse was constructed in 1904 along the shores of St. Mary’s Bay. One of the few surviving Nova Scotian lighthouses with the keeper’s residence attached, it was decommissioned in 1984 and is now preserved as a museum and provincially registered heritage property. Thanks to the Paterson’s for sharing.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Inflation worries surge

Global oil prices surged once again on Monday morning after the U.S. and Iran traded military strikes over the weekend. Peace talks broke down at the end of last week, seemingly leading to an escalation of the conflict. The rising price of oil will have a significant impact across the global economy. It will likely lead to higher prices and, in turn, a higher inflation rate. Higher inflation will result in interest rate hikes from global Central Banks, including the Federal Reserve.

Before this conflict began, traders forecasted one interest rate cut this year; now, the consensus forecast is for one to two hikes. The CME Group’s FedWatch pegs the odds of a July hike at just 31.5% but sees the chances of an increase in September at more than 68%, with the probability of a follow-on move higher by the end of the year, trading at just under 50%.

We will have to see what the FED does, as a hawkish FED could topple markets, while a dovish FED could allow inflation to remain a problem.

This all comes at the start of a very important week for Wall Street. Federal Reserve Chairman Kevin Warsh is due to give his first congressional testimony on Tuesday, and the Bureau of Labor Statistics will release key inflation data earlier that morning. This week also kicks off a key earnings period with many companies reporting over the next few weeks. This week’s earnings are highlighted by numerous Wall Street banks, including Wells Fargo, JPMorgan Chase, Regions Financial, and Bank of America.

These worries and military strikes led stocks lower on Monday morning. It has surely been a rocky market over the last few weeks.

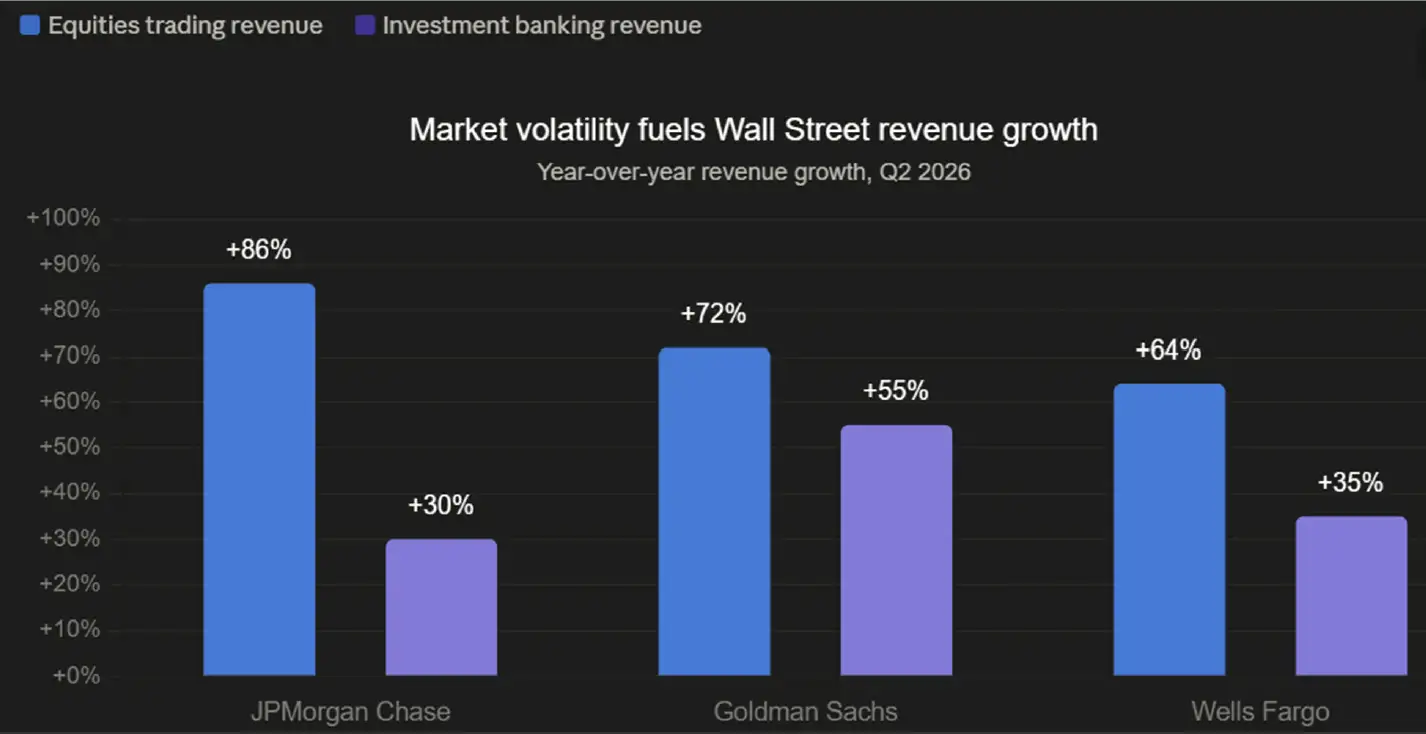

Wall Street Banks benefit from market volatility

Major U.S. banks reported strong second-quarter results, supported by increased trading activity and a rebound in investment banking. Market volatility, renewed merger activity, public offerings and significant corporate borrowing all contributed to higher revenues across the sector.

The results demonstrate that volatility is not universally negative. While uncertainty can weigh on financial markets and investor sentiment, it can also create opportunities for businesses positioned to benefit from increased trading, financing and dealmaking activity. However, strong bank earnings do not eliminate the broader risks associated with high valuations, inflation and tightening credit conditions.

It’s worth noting, however, that this is a different business than ours. Investment banks earn more when markets move, when deals get done and when clients trade. Their revenue is tied to activity itself.

As an independent portfolio manager, our compensation comes solely from management fees, not from transactions. We don’t benefit from market uncertainty — we exist to help you navigate it. There is no incentive on our end to trade more when markets are volatile. Our interests are aligned with a simple goal: protecting and growing what you’ve built, so that uncertainty never becomes a problem to manage alone.

Credit conditions impacting hyperscalers

According to Jeffrey Papai of Goldman Sachs, artificial intelligence giants require $1 trillion in financing over the next year. This comes after the same firms used $360 billion to fund their AI investments last year.

These major cloud infrastructure providers are reportedly facing financing challenges due to tight credit conditions. For years, these firms did not require financing due to their strong and substantial cash flows. AI changed that as they burned cash, resulting in massive credit and equity raises. However, it seems that investor fatigue is setting in, and even the large hyperscalers will have difficulty raising capital in today’s market.

According to Bloomberg, Amazon, Alphabet, Nvidia, Meta, Oracle, and SpaceX have issued a combined $182 billion in investment grade bonds this year, a 1,300% increase YoY. As a result, these firms account for nearly 15% of total U.S. corporate bond issuance year-to-date and more than 50% of this year’s growth in corporate bond issuance.

The broader credit market is already seeing increased defaults, liquidity issues, and decreased investor demand. The market remains tight even for the most high-quality issuers like Microsoft and Amazon. While tech companies have traditionally enjoyed top-tier credit ratings, the unprecedented borrowing pace is causing credit spreads to widen for AI issuers. We simply do not think the math adds up, and the market agrees.

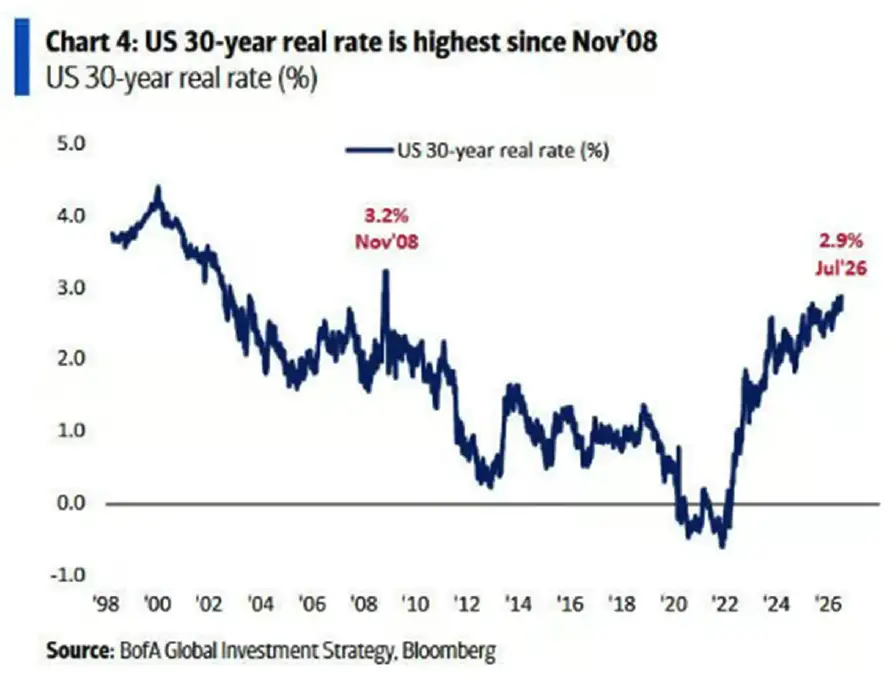

It seems the funding window has closed for now; we will have to see whether that changes. If rates remain elevated, we expect these issues to persist and many of these hyperscalers to potentially cut their spending forecasts. Currently, U.S. long-term real interest rates are at their highest level since the financial crisis.

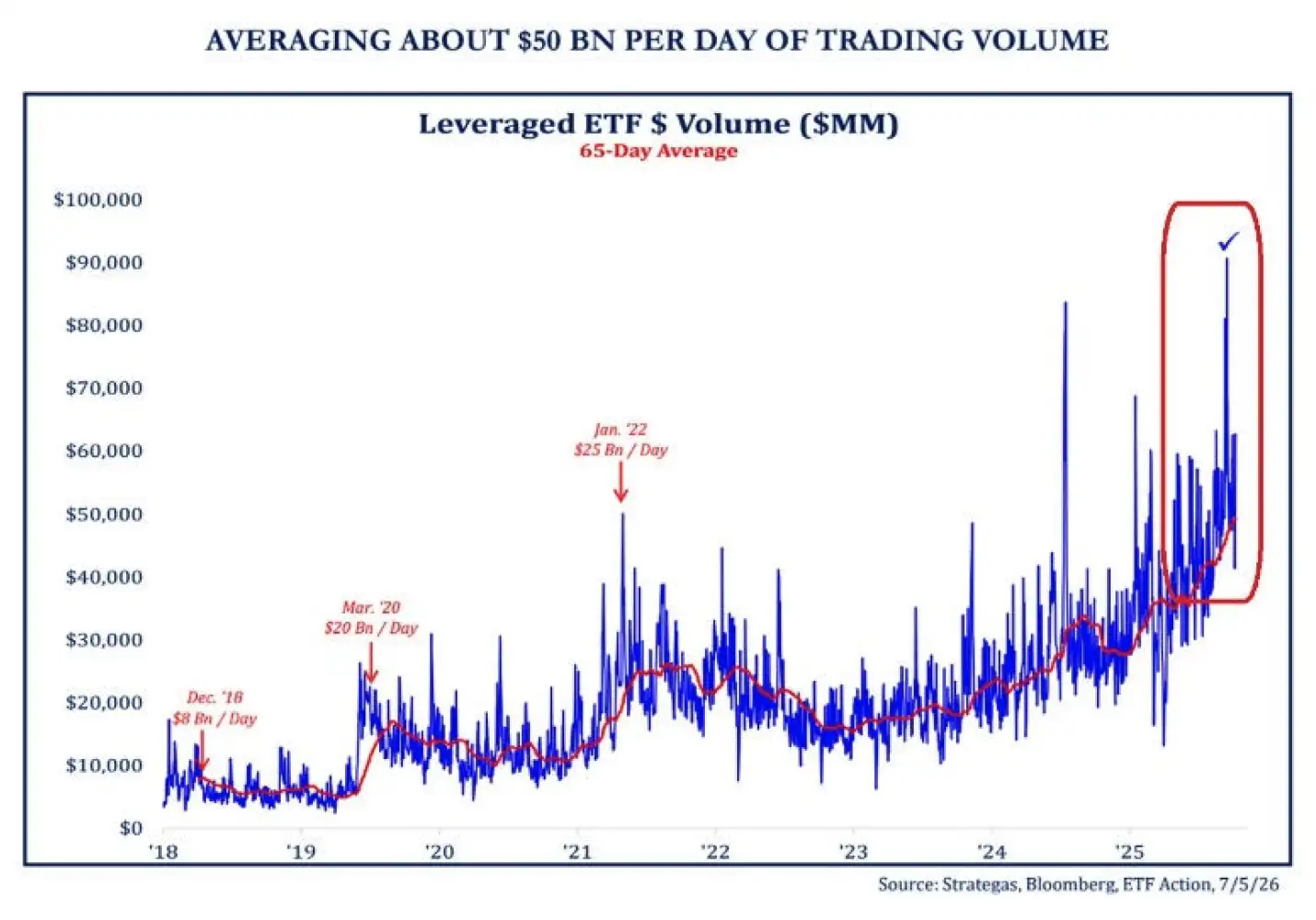

Risk factors continue to emerge across financial markets and the economy, and we want to stay ahead of the herd that continues to pile into equities like it’s the early stages of a bull market.

We like to use leveraged ETF trading volume as a gauge of market sentiment and retail allocation. Currently, the 65-day average for leveraged ETF volume is at an all-time high and sits at a level that is triple the 2021 meme-stock peak. Average trading volume has more than doubled over the last two years:

Most of these leveraged bets are long, as the ratio between leveraged long and short ETF volumes is up to 4.5x, the highest since 2021.

Leveraged trading has never been so popular and has been fully embraced by retail investors. For those of you who do not know, leveraged ETFs enhance the return of a traditional ETF. Many of these leveraged ETFs invest in the highest-growth areas of the market, such as space exploration, artificial intelligence and data centers. There are also single-name leveraged ETFs that enhance the return of a single stock through the use of leverage. We would warn our readers that, during down markets, leveraged ETFs can substantially underperform, something we think retail investors are completely ignoring.

What we are looking at next week:

Markets enter the week of July 20th with investors somewhat buoyed by encouraging inflation data after both June CPI and PPI reports came in below expectations, reinforcing the idea that price pressures may be easing. The softer-than-expected readings helped support equity markets and renewed optimism that the Federal Reserve may have greater flexibility with regards to interest rates in the months ahead. Attention will likely now shift away from economic data and towards the technicals, as the S&P 500 is less than 1% away from new all-time highs after consolidating for most of the last 2 months. The question will be whether this positive inflation data is enough to push the index higher on its own.

Second-quarter earnings season will continue to loom large in the background, with several large technology, industrial, and consumer companies set to report throughout the week. Investors will be looking for signs from management that corporate earnings continue to justify high valuations, particularly following another quarter of robust AI-related investment. At the same time, as mentioned, markets remain technically well-positioned after the post-inflation reading reaction. At this point the question will likely shift towards monitoring whether market leadership can sufficiently broaden out beyond the large-cap tech/AI companies or remain concentrated in the same handful of companies responsible for much of this year’s rally.

MacNicol & Associates Asset Management

July 17th, 2026

Download in PDF format:

{kind=link}