We will be giving some macro economic market updates on a weekly basis. No equity recommendations will be given in this commentary, and we encourage you to contact us if you have questions regarding any observations.

Feel free to send in your pictures of lighthouses to be featured in our weekly commentary.

BEACONS OF THE WEEK

The two main purposes of a Lighthouse are to serve as a navigational aid and to warn ships (Investors) of dangerous areas. It is like a traffic sign on the sea.

Kõpu Lighthouse, Hiiumaa, Estonia

Kõpu Lighthouse, Hiiumaa, Estonia

Kõpu Lighthouse is very famous lighthouse in Estonia that is visited by thousands of tourists per year. The lighthouse was constructed in 1531 and stands at 124 feet tall. The lighthouse was automated in 1963. The lighthouse has a range of 48 kilometers.

Boston Light, Little Brewster Island, Boston, Massachusetts

The Boston Light was built originally in 1716, the current lighthouse was built in 1763. The second iteration of the Boston Light is the second oldest lighthouse in the U.S. The lighthouse was automated in 1998 and stands at 89 feet tall.

The Boston Light was built originally in 1716, the current lighthouse was built in 1763. The second iteration of the Boston Light is the second oldest lighthouse in the U.S. The lighthouse was automated in 1998 and stands at 89 feet tall.

Peloton’s savior?

Has Peloton found a savior? The American exercise equipment and media company has

been on a roller coaster ride since going public in 2019. The company saw its share price explode during COVID-19 before subsequently collapsing by more than 95% since January 2021. The company has gone through new leadership teams, sales rumors, soft sales, and numerous other issues. The company that could face bankruptcy seemingly got some good news this past week as it was rumored that numerous private equity firms were looking to buy the company. According to a report by CNBC on Tuesday, several private equity firms are looking to buy the company out as they work to refinance their debt and cut costs. The potential buyout would make the company private again.

News of this buyout made Peloton shares jump by more than 10% on Tuesday morning as investors finally had some optimism. Peloton shares are still down 31% year-to-date despite this bounce.

Last week, Peloton announced a broad restructuring plan that’s expected to reduce its annual run-rate expenses by more than $200 million by the end of fiscal 2025.

However, despite the report, there is no guarantee of the deal. A Peloton spokesperson declined to comment on the rumored buyout citing that they do not comment on speculation or rumours.

Peloton has a profitable subscription business with millions of loyal users but has been hamstrung by their equipment business which originally made them a household name in the fitness world. Peloton has seen softer demand for their equipment as consumers have decreased their at home fitness spending. The company has also had to face numerous recalls on certain models of their bikes and treadmills.

Over the last 2+ years, shareholders have sold Peloton in droves as the company has struggled to grow sales, generate free cash flow, and chart a path to profitability.

Peloton is currently in talks with JP Morgan and Goldman Sachs to restructure its debt

which includes a $692.1 million term loan due as early as November 2025 and $991.4 million on its 0% convertible senior notes due in February 2026. Reportedly the company will not have an issue restructuring the debt.

We think Peloton belongs private until a pathway of profitability and stability is clear. The company went public too early on hype and speculation. Insiders sold and shareholders have been holding the bay down. We are glad we completely avoided this company.

Like the Magnificent 7

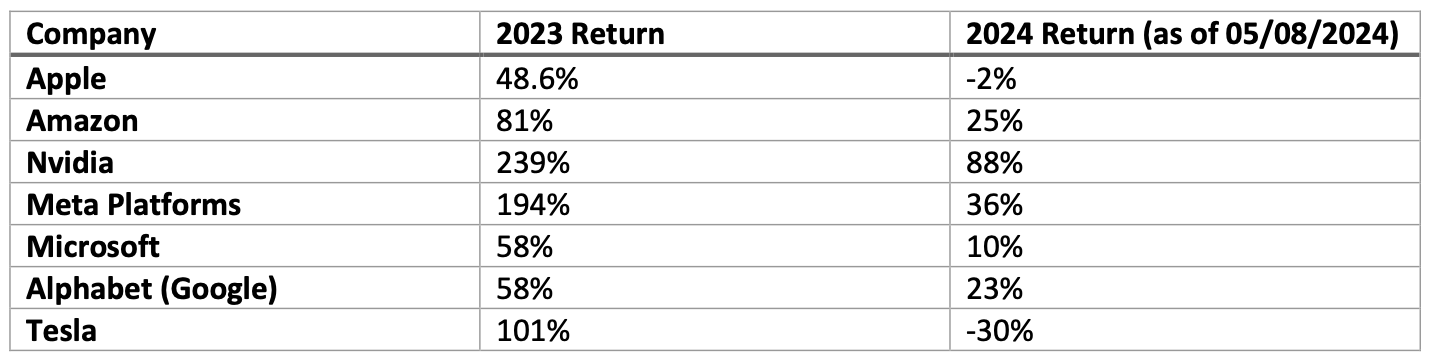

We have talked in recent editions of the decoupling of the Magnificent 7, seen in recent months. For over a year, the mega-cap Magnificent 7 carried markets with massive returns. Fast forward to today and not all Magnificent 7 members are performing equally.

While Tesla shares have lagged, other Magnificent 7 stocks have continued to surge. Apple shares have also struggled this year despite recently bouncing. Yhey are trading 9% off their 52-week highs. We believe the Magnificent 7 has become, at least for now, a Fabulous 5. The same can be said for the G7 which is why we bring this all up to you this week.

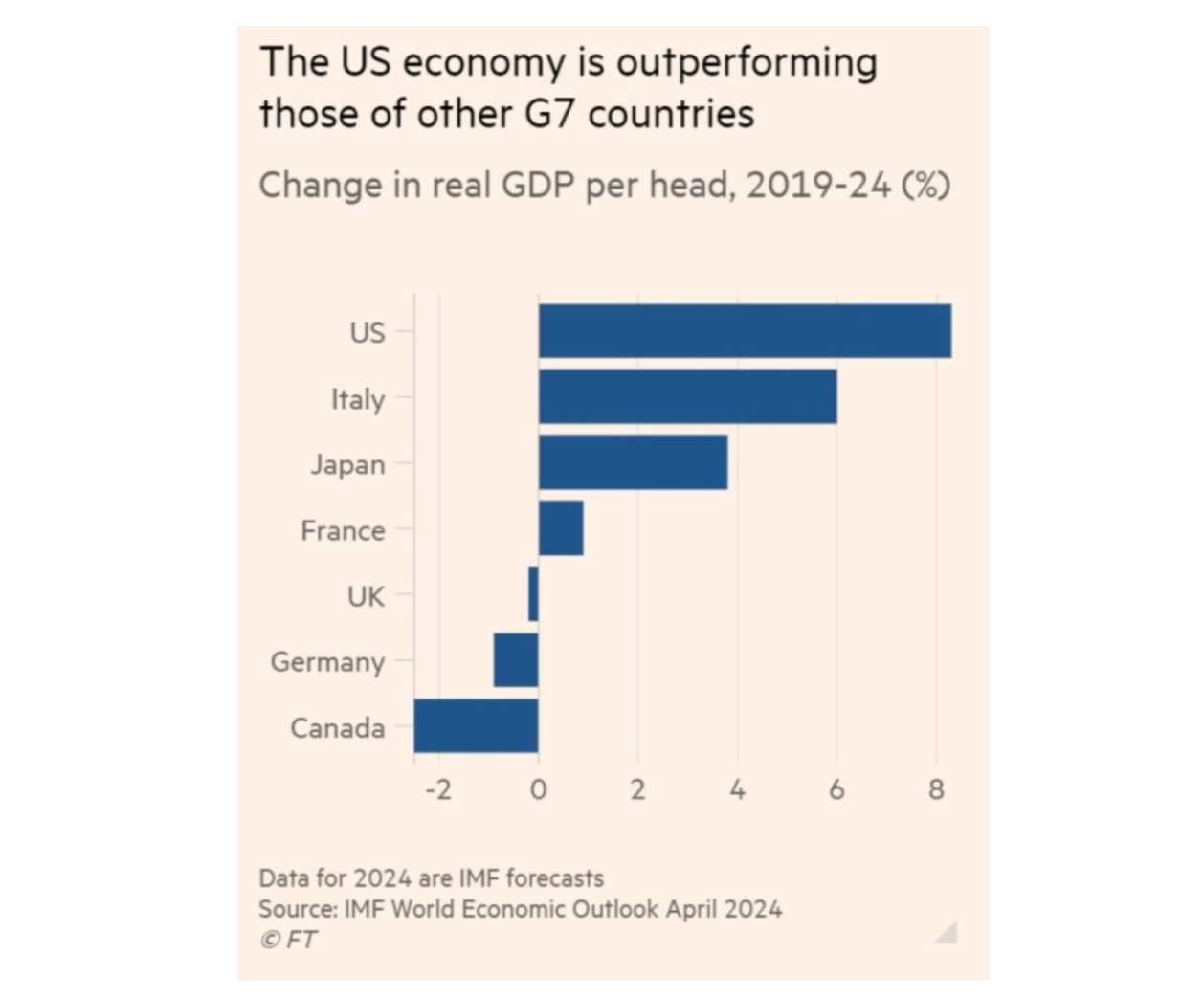

As you all know, the Group of Seven is an intergovernmental political and economic forum consisting of Canada, the U.S., Japan, the U.K., France, Germany, and Italy. The countries share many attributes including being major advanced economies.

However, all these developed economies were not created equally…….

According to the IMF, Canada has severely lagged its G7 compatriots in terms of GDP per capita growth over the last 5 years. GDP per capita has contracted in Canada by close to 2% between 2019 and 2024. When you compare Canada’s number to its big brother down south, the U.S. is lapping us above the border.

So why is that? Americans have been more productive over this period. Canada has artificially boosted its GDP growth number through immigration. The U.S. regulatory and legal environment is much more pro-business than Canada, and many talented, and intelligent Canadians have hit the road and immigrated away from Canada for various reasons. Another major reason is that the U.S. is the global hotbed of technological innovation, no matter the sector, and Canada is nowhere close. Hopefully, if you are Canadian, you owned some U.S. Dollar assets in recent years and we recommend you continue to do so……

As Canadians, we hope the leaders of this country finally address and solve this issue as it seems the quality of life for many across this country has slipped in recent years.

King of bonds, turns on them

The ‘King of Bonds’ Bill Gross, the co-founder of Pacific Investment Management Company (PIMCO), a global fixed-income investment company has declared that bond funds are dead. The billionaire gained his wealth by selling bond funds to the masses.

This week he gave an interesting statement that caught our eyes. In an essay he authored and posted on his website, Gross says the math in bonds is no longer in the investor’s favor. Gross and PIMCO promoted the notion of ‘total return’ in bonds,promoting that investors should focus on both interest income and capital appreciation like stocks.

When Gross popularized the total return idea in the 1980s, treasury yields were 15%. There has been a huge tailwind for capital appreciation in bonds since then as rates rapidly declined from 1980 to 2020. Today, there is a lot less room for error as treasury yields are yielding 4.5%.

Gross said in his essay that bond bulls have been arguing that rate cuts will reverse the capital appreciation losses that we have seen in the last few years rapidly, but he believes that investors should not count on that outcome. He argues the fast-growing supply of Treasuries will make it very difficult for long-term bonds to sustain a price rally, no matter what the FED does. He goes on to say that total return is dead and to not let them sell you a traditional bond fund.

Gross pointed to the Vanguard Total Bond Market Index Fund in his essay citing that bonds have not just had poor returns in one or two years. He points to the fund’s negative annual return over the last half- decade. The bond fund has returned -0.12% per year over the last 5 years. He goes on to say that 5 years is a long time in retirement and bonds are not proving the safety that they are supposed to for retirees.

Gross’s essay is something that we agree with and have known for quite some time. It is why we have avoided long-term bonds for quite some time and believe short-term securities are the only option currently. The yields that the money market and very short-term bond funds are paying are attractive in this space and are less impacted by the phenomenon that Gross spoke of.

If your portfolio has underperformed in recent years, we would guess that the fixed income portion of the portfolio has been a root cause of this. We think a blended approach to investing is needed for both retirees and investors still working.

Contact us today at info@macnicolasset.com to talk with one of our portfolio managers who can overview the bond market and explain more about why you should avoid bonds, especially long-term ones.

Bitcoin funds, large outflows

Bitcoin hit an all-time high price of $74,000 in mid-March. Since then, the price per coin has dropped to approximately $62,000. Bitcoin ETF approvals from the SEC and the halving event in April for Bitcoin were supposed to be huge tailwinds for the asset that would send it to new heights.

However, prices have retreated, and investors have seemingly taken some money off the table in the space.

Approximately $710 million has flowed out of Bitcoin ETFs over the past week, according to Dune, a cryptocurrency data platform. Overall, Bitcoin ETFs have still had $11.1 billion in inflows since their launch. The products are popular, but we believe many in the industry overestimated the retail interest in the space.

In addition to the challenging market conditions for risk assets like Bitcoin, these outflows are typical with newly launched ETFs according to Bloomberg. According to Bloomberg’s Senior ETF analyst, this recent drop for Bitcoin will remind retail investors that Bitcoin is extremely volatile and not an equivalent store of value like gold, which he suspects some wholesalers of the ETFs may be selling to clients. Bitcoin is a speculative asset that has high risk. We believe if you want to take exposure, it should be in the low single digits in terms of percent of your total assets. Nobody wants to see their retirement savings disappear over the next Bitcoin bear market despite their belief in it.

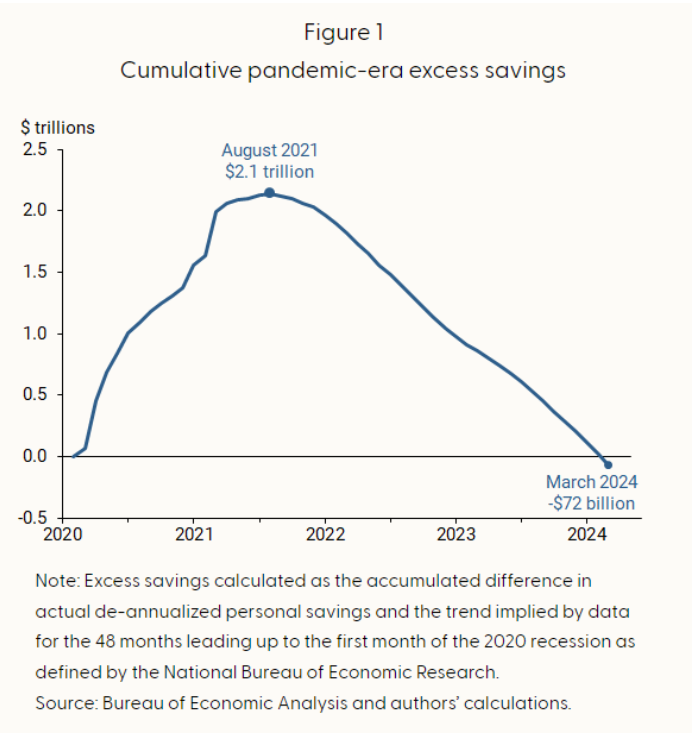

Excessive savings disappearing act

When Covid-19 started countries printed trillions and provided all kinds of support for consumers, businesses, and partnerships. All this money was not spent initially by consumers. Many used this government support as savings. If you remember back in early 2021, it was when every person in the world (it seemed) was day trading and investing on their own. This phenomenon led to the birth of meme stocks, retail investors buying SPACs, and Twitter investing “gurus”. The whole era was fueled bygovernment stimulus cheques.

Fast forward 3 more years and all that excessive savings has disappeared.

According to the Bureau of Economic Analysis, pandemic-era excess savings in the U.S.

have disappeared and caused consumers to draw from other funds. At the height, there

was approximately $2.1 trillion in excess savings in the U.S. American consumers have

fueled their lifestyle over the last 2.5 years by spending that extra money that they saved

in the initial days of COVID-19. Is this sustainable? No. Is this a warning that there could be trouble under the hood for many consumers? We think so.

We know the money has not disappeared. It gets recycled through the system and eventually is spent again.

This chart is a major reason why stocks like Lululemon and Nike have struggled recently. Consumers are spending less, especially on non-necessity goods, and it is impacting these companies’ sales and growth numbers. If somebody you know recommends one of those stocks or some other goods-focused enterprise that produces non-necessity goods, we recommend showing them the chart above as a reason why that could be a bad idea in the short term.

U.S. revokes chip licenses

The U.S. government revoked licenses to sell semiconductor chips to China’s Huawei. Intel and Qualcomm were the two companies that saw their licenses revoked. Intel declined to comment on whether the customer they lost their license to was Huawei while Qualcomm confirmed that was the company.

Both companies have said they will comply with U.S. regulations. Intel announced they believe Q2 revenue will come in at the low end of their original guidance range. In 2023, China accounted for 27% of Intel’s revenue, with 6% of revenue dependent on export control authorizations. China accounted for a whopping 62% of Qualcomm’s revenue last year.

After this news report, both chip makers saw their share prices drop. Numerous analysts believe that Intel will be more impacted without this license as Qualcomm’s sales to Huawei have recently become quite minor.

This is a reminder that even though the industry could be the future, relying on sales to China presents you with an added risk as a company and as an investor in that company.

NFL and private equity

Two things that are very prevalent in Murray Hill in New York City, are new grads who love football and that work in private equity. This week the two things linked up in some hot news.

The NFL officially approved a plan that will allow NFL ownership groups to sell as much as 30% of their teams to private equity groups. The proposed rules would allow buyout firms to acquire up to 10% of a team according to people familiar with the matter. The NFL owners are set to discuss these potential changes at their ownership meetings in mid-May.

Some private equity firms have been quite active in buying parts of sports teams in

recent years including RedBird Capital Partners (Fenway Sports Group), Arctos Partners (numerous teams across Big 4 leagues), and Ares Management Corp (Ottawa Senators, San Diego Padres).

The process to buy an NFL team has historically been much more rigorous than the process for NBA, NHL, and MLB teams. NFL teams also fetch the most on the open market by a wide margin. Reportedly the process will remain quite difficult and private equity firms looking to buy a piece of an NFL team will still be heavily vetted.

The NBA currently caps private equity ownership at 30% of a team, while a single fund can only own 20% of a franchise, and funds are limited to a maximum of five teams.

We think this is a very interesting story and cannot wait to see what happens. Owning NFL teams has been one of the strongest investments over the last 40-50 years. We think investors will be salivating at an opportunity to ‘own’ a franchise.

{kind=link}

{kind=link}