Amrum Lighthouse, Amrum Island, Germany

This lighthouse is located in the North Sea in the German state of Schleswig-Holstein. The lighthouse was built in 1873 and was automated in 1984. The lighthouse is a heritage monument in Germany.

Dagebull Lighthouse, Dagebull, Germany

This lighthouse is a retired lighthouse in northern Germany. The lighthouse was originally constructed in 1929 and was deactivated in 1988. As of 2018, the lighthouse was being used as a hotel room for 2 guests.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Stocks pull back

Last Friday and on Tuesday, stocks pulled for the first time in what feels like weeks. Stocks pulled back due to the escalating U.S. – China trade war. On Friday, $2 trillion in market value was wiped out, and the S&P 500 had its worst session since April. These were caused by a single social media post from the President. Trump wrote that China was becoming very hostile and accused the country of holding the world “captive” due to its monopoly on rare earth metals. He also stated that China was hurting the world’s economy by monopolizing rare earth metals. Trump went on to say that his administration is looking at policies to increase tariffs on Chinese products. This sent markets downward, with chipmakers and technology companies leading the way.

Trump knows the U.S. and the West are at the whim of China when it comes to rare earth metals. That is why his administration is investing in the sector and is looking to decrease its dependence on China.

Trump’s threats were sparked by a move from China on Thursday night of last week. Beijing stated that outside entities must obtain licenses to export any products containing rare earth metals, and that companies using the metals for military applications would be denied.

Even though progress has been much slower in regard to trade discussions between China and the U.S. compared to other U.S. trade partners, investors had begun to believe a deal would happen, and the relationship was thawing between the two superpowers. President Trump and Xi are also set to meet at the APEC summit at the end of October. Trump threatened to skip the summit in his posts. If Trump follows through with his latest threat (raising China’s tariffs above 40%), investors fear that the load may be too great to bear for the U.S. economy, which is still reliant on imported parts to build automobiles, solar panels, and the like.

After the market had a negative reaction to this post, Trump tried to tone down the rhetoric over the weekend. Secretary Bessent stated that China and U.S. officials continue dialogue in regard to trade and that Trump would still be in attendance for the APEC summit in South Korea. Trump also stated on Sunday that he respects Xi and said Xi had a bad moment. He went on to say, “Don’t worry about China……the U.S.A. wants to help China, not hurt it!!!”.

It is no surprise that Trump walked back his rhetoric; the stock market is one of his major indicators for measuring his administration’s success. After walking back his comments, the S&P 500 jumped over 1.5% on Monday, its best day since May 27th.

After Monday’s rebound, more China news caused whiplash across financial markets after China put sanctions on 5 U.S. subsidiaries of the South Korean firm Hanwha Ocean. China will essentially start charging additional fees on cargo ships and impose further sanctions on select U.S. shipping subsidiaries. China also blamed tensions over the last week solely on Trump and the U.S.

Chinese stocks pulled back over the last week with these rising tensions. On the other side, safe-haven assets like gold, Treasuries, and the U.S. Dollar rose as investors look to safety as risks rise across markets. Trade discussions between China and the U.S. are not the only major risk across markets; the U.S. government remains shut down, and geopolitical tensions continue. We have also entered earnings season, where investors will be paying close attention to how the economy has impacted company earnings, revenue, and forecasts.

Beyond bizarre

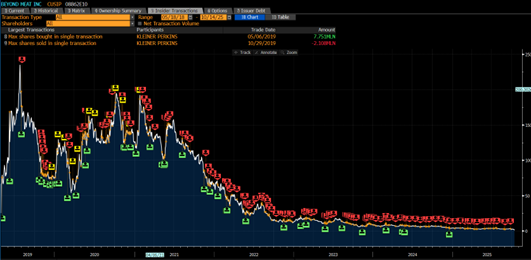

This week, we personally wanted to highlight a milestone for Beyond Meat, the popular protein alternative producer. Once a darling of Wall Street, the company’s shares now trade below $1/share. Beyond Meat shares went public in mid-2019 and shares immediately surged. Consumers and investors believed in the plant-based meat alternatives company that was founded in 2009. After all, in 2019, the company had partnerships with major grocers and even fast-food chains. The runway looked real.

Beyond Meat went public at a valuation of $1.46 billion, raising $240 million in May 2019. On its first trading day, shares surged by 163%. In the coming months, shares surged, increasing Beyond Meat’s valuation to $15.6 billion by the end of July 2019. After that, shares cratered by almost 70% before the end of 2019 and the start of 2020. However, shares returned to near all-time highs during the growth surge that we saw in late 2020. However, since then, shares have cratered to below $1. Beyond Meat’s market capitalization is now only $62 million (1/4 of what they raised in their IPO). Shares tanked by 23% on Tuesday (and are down 77% this year) when the plant-based meat producer announced a debt swap deal that would reduce the company’s debt by $800 million but increase the common share count by over 400% (talk about dilution). According to the terms of the deal, Beyond Meat will receive $202.5 million in debt due in 2030 in exchange for debt maturing in 2027. Around 97% of the holders of its convertible notes agreed to the terms of this exchange. The original announcement for this debt swap was made a few weeks ago, but it was confirmed this week.

Beyond Meat has struggled with debt, has never turned a profit, and has even seen its revenue decrease in recent years. The company has raised $100s of millions of dollars in equity and has washed it away. Sell-side analysts slashed price targets for Beyond Meat this week, stating that the firm remains “operationally and financially challenged”. However, at one point, Wall Street loved this company. It was a consumer product that was rapidly growing and raising millions.

In recent months, insiders have been rapidly selling shares. This chart from Bloomberg that tracks insider buys and sells is quite glaring, and there is a BIG trend that began basically in mid-2021 and has continued for over 3 years now:

Retail investors got caught holding the bag, and numerous insiders cashed out.

For now, Beyond Meat avoids insolvency, but this is one that we would recommend a major stay away from for our readers. The firm is burning cash, and its market share has decreased over the last 3-5 years.

I brought this up as the author this week because for me, this is a full circle. In July 2019, I was taking an upper-year valuation class, the class taught us all about valuation techniques and modelling. In the class, we had to value two companies for two different projects. One of the companies I analyzed was Beyond Meat (the company was on fire at the time). My analysis, which I had to justify to my Professor, indicated a strong sell rating for Beyond Meat. For curiosity purposes, I looked around my personal computer for this model and found it this week. My DCF (Discounted Cash Flow Model) punched out values between $25.61 and $131.37 with a base case of $58.66. Shares were trading at this time above $150. Over a long time, I thought my analysis was flawed as it was not “consensus”; however, my critical and contrarian thinking at this time allowed me to paint a clear and unbiased picture for Beyond Meat.

Personally, we are all glad we did not buy the hype when it came to Beyond Meat in 2019. We also think this non-consensus thinking continues to benefit our investors and portfolio returns. We are not indexers, and we do not follow the herd. We think our portfolios are diversified in a way that can perform in any type of market environment. We also believe our portfolio drawdowns and risk metrics relative to many “consensus” investors are much lower.

In today’s market environment, it is extremely important not to fall asleep at the wheel and find solutions that will work tomorrow, not the ones that worked yesterday. We think this thinking will benefit our investors moving forward, no matter what the risks that are present across financial markets.

JPMorgan makes a splash

Over the last few days, JPMorgan made a huge announcement that it will invest $1.5 trillion into 27 critical industries in the U.S. These industries include critical minerals and processing, battery storage, nuclear energy, shipbuilding, solar, 6G, sensor hardware, and more.

JPMorgan has coined this initiative, the security and resiliency initiative, to boost critical industries. The firm will make direct equity investments of up to $10 billion as part of the initiative. The company stated that the deal will include middle-market companies as well as large corporate clients. The 10-year plan will facilitate, finance, and invest in industries critical to national economic security and resiliency. Jamie Dimon stated that this plan is not Trump-driven; it’s 100% commercial.

This announcement comes as national economic security has become a focus of many countries across the world, China and the U.S. spar on trade, and the U.S. government makes direct equity investments in critical mineral companies.

We think this is yet another tailwind for many industries we are invested in, including metals and mining, and energy. The announcement from JPMorgan comes as the company announced earnings on Tuesday.

We think these critical industries will continue to receive funding and focus from Western governments, especially as the separation of the global economy continues to unfold. We also think this investment signals something that we have been forecasting for quite some time, a commodity Supercycle which will be driven by inflation and the AI investment wave that is being driven by capex spending from technology companies, and semiconductor producers.

Speaking of earnings

This week marked an important week for the financial sector; many Wall Street firms reported their earnings. Over this past week, JPMorgan, Wells Fargo, Goldman Sachs, BlackRock, Citigroup, Bank of America, Morgan Stanley, and a few insurance providers all reported their earnings. All the companies that we directly mentioned in the sentence before beat revenue and earnings estimates. Most of these firms beat revenue and earnings estimates every quarter; however, the piece we noticed is how strong these quarters’ numbers were. Some metrics smashed expectations and surged year-over-year (Bank of America profit jumped 23%, Morgan Stanley revenue jumped 18% driven by a surge in dealmaking and strong growth numbers in their wealth management unit, and Goldman Sachs profit surged 37% driven by sales and trading, and money managers).

Wall Street’s strong earnings offer an encouraging picture as economic fears continue to linger and plague markets. The banks’ earnings showed key measures for consumer health (ie. Credit losses and spending), are holding up in the face of broad economic concerns and a weak labor market. Analysts and investors were looking at specific line items from these earnings reports to gauge overall economic health across the country.

On a negative note, JPMorgan’s top dog, Jamie Dimon, warned investors about the bankruptcies of two auto companies in recent weeks. Numerous Wall Street firms were exposed to Tricolor Holdings and First Brands when they announced their bankruptcy filings. Dimon called the two recent bankruptcies (JPMorgan only had exposure to one of the companies and had to write down $170 million during Q3) “cockroaches” and said more will emerge as the private credit sector deteriorates and weak links are exposed across the sector.

Private credit firms are not directly regulated and are not forced to disclose the level of risk on their books. Regulated banks like JPMorgan are exposed to the sector either by lending to the private credit firms or the private businesses that are backed by private credit.

Dimon went on to say that JPMorgan made mistakes like the rest of the industry but is scouring its data to expose any other underlying issues. He called his company’s $170 million write-down “not our best moment” regarding the two auto firms’ bankruptcies. Dimon also warned investors in regard to private credit and claimed that more of these bankruptcies will pop up as the economy breaks down in a downturn.

In regard to economic conditions, Jamie Dimon stated that a resilient consumer is one of the reasons firms continue to report strong earnings.

In 2025, JPMorgan shares are up 28%, Bank of America shares 19%, Wells Fargo 22%, CitiGroup 42%, Morgan Stanley 32%, and Goldman Sachs 35%. It has been quite a strong year for financials across North America; numerous Canadian firms have also been on quite a run.

MacNicol & Associates Asset Management

October 17

Download in PDF format:

The Weekly Beacon October 10 2025 US

{kind=link}