This commentary was written by our team and NOT outsourced to a third party. We will be giving some macro-economic market updates on a weekly basis. No equity recommendations will be given in this commentary and we encourage you to contact us if you have questions regarding our observations.

Colchester Reef Light, Lake Champlain, Vermont

This lighthouse was a lighthouse off Colchester Point in Lake Champlain from 1871 to 1933. The lighthouse was moved in 1956 to the Shelburne Museum in Vermont.

Fire island Lighthouse, Fire Island Inlet, Long Island

This Long Island lighthouse is a visible landmark in southern Suffolk County, New York. The lighthouse was originally built in 1826 and was automated in 1986.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Chinese optimism

Over the weekend, U.S. and Chinese officials met in Geneva, Switzerland, to discuss trade between the world’s two largest economies. Trade discussions reportedly went very well, and according to statements from both sides, the framework for a deal has been outlined. For the time being (90 days), U.S. tariffs on Chinese goods will be reduced from 145% to 30%. Chinese duties on American goods will also drop to 10%. According to statements from officials involved in the negotiations, the two countries will work to solve the trade deficit between the two countries in the coming months.

Despite the positive news from these meetings, do not expect tariffs to return to normal. Secretary Bessent stated that it is implausible that tariffs on China will ever go below 10%. Bessent also stated that a call between President Trump and President Xi could occur over the next few weeks. In an interview on CNBC on Monday morning, Secretary Bessent stated that the trade agreement from the weekend represents progress in America’s strategic decoupling from China. Bessent and Trump do not want an overall decoupling from China; they want a strategic one in vital industries and necessity goods.

Ever since Trump enacted tariffs on American trade partners, the steep tariffs on China have been worrying investors the most, as a resolution looked improbable and tensions between the two looked like they were worsening.

In a statement, Trump acknowledged the weekend discussions, stating that the U.S. has achieved a total reset regarding trade with China.

Markets surged on Monday morning on this news as investors piled into riskier assets. Tech stocks, oil, consumer goods stocks, and treasury yields surged on this news. Small caps even got in on the action, hitting 6-week highs on Monday morning. The price of gold, consumer staples, and low-risk assets moved lower. Although this news is bullish, we are not ready to go all in on high-risk growth, we still believe there are numerous risk factors across the global market, and assets like gold, utilities, and consumer staples still belong in our investors’ portfolios.

We are not sure how and when an official decoupling will occur, but we believe it is inevitable as the West and East continue to move further apart. Bessent also indicated that Chinese officials acknowledged the American epidemic on fentanyl and will work with the U.S to stop the flow of the lethal drug.

Mark Williams, Chief Asian Economist at Capital Economics, described the trade war truce as “a substantial de-escalation.” These discussions being so positive surprised many analysts who thought discussions would take much more effort and time between the two countries.

Regardless of how you feel regarding China or Trump, these discussions are positive and could serve as an early example of how the West can create trade agreements with China moving forward. We will also say that this progress between the U.S. and China somewhat takes the worst case off the table in regard to global trade risk.

Buying the dip

The price of uranium and uranium miners have pulled back over the last 8-12 months after a 2-ish year bull market. For those of you who have read our commentary for a few years now, you know we were early in the trade and have not sold off our holdings in the sector despite the pullback in prices. We remain very bullish on nuclear energy and believe the price of uranium will begin its next move up. On the demand side, we continue to see bullish news monthly. Countries are committing to building nuclear reactors, countries are classifying nuclear energy as ‘green energy’, companies are investing in nuclear energy to secure electricity, and the U.S. government is committing to nuclear energy. The bullish signs are all over the place on the demand side.

At the same time, we continue to see disruptions on the supply side, which furthers our thesis that supply will not be able to meet global demand moving forward. This week, Kazakhstan’s largest nuclear project was stalled due to an internal dispute between shareholders over the choice of a contractor.

Supply disruptions are widespread and are impacting both small and large producers. We think this will continue, and the supply imbalance will expand.

Uranium prices have been on the rise in recent weeks as they look to have broken their multi-month negative trend.

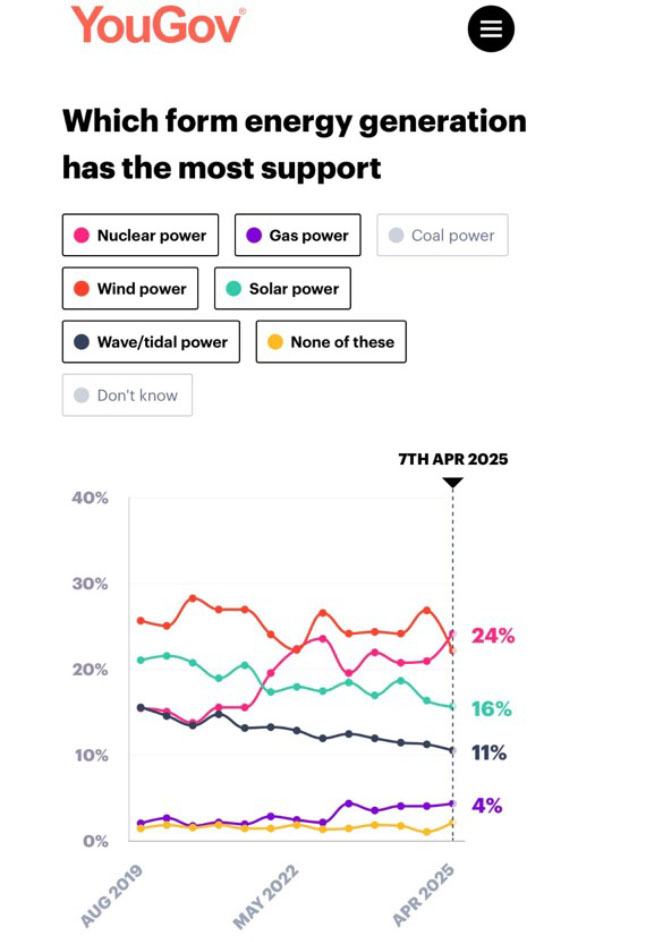

Public support is even swinging in nuclear energy’s favour as green supporters and energy traditionalists both think nuclear energy is the future. In the UK, nuclear energy has the most support according to a poll by YouGov. Just 5 years ago, it was the 4th most supported energy source by the public.

The tide is changing.

Disclaimer: MacNicol & Associates Asset Management holds shares of uranium miners and physical uranium across various client accounts.

Global conflict discussions

Over the weekend, the U.S. Department of State announced that it had brokered a cease-fire between India and Pakistan, which broke out into a conflict earlier this month. The conflict had the world watching as both nations have nuclear weapons, and tensions have been on the rise between the two nations. The recent tensions stem from a terrorist attack on Indian soil that killed 26 civilians in April. The attacks were reportedly perpetrated by a Pakistan-based terrorist group. Pakistan has denied these claims and blamed India for the attacks.

This ceasefire is a positive step for the conflict. The conflict had the potential to escalate and disrupt global supply chains.

In other conflict news, the Presidents of Ukraine and Russia will reportedly meet in Turkey on Thursday. In what could be a monumental meeting, tensions could be slowing down between the two nations. The three-year conflict has had no cooperation from either side. According to European Reporters, the meeting will require both nations to agree to a 30-day ceasefire. We will have to see how this unfolds, but we are optimistic about the progress being made. We hope that these conflicts can be resolved as the parties most impacted are the citizens of each nation involved.

Cool inflation

On Tuesday morning, investors woke up to some great data from the Bureau of Labour Statistics. April’s inflation report was released, and it showed inflation cooling even more despite some tariffs being in place. Year-over-year inflation came in at 2.3% versus a 2.4% estimate from economists. Both Core and Headline CPI for April also came in lower than economists’ expectations. Futures rallied on Tuesday morning on this positive news.

Energy prices moved higher in April despite the recent drop in the price of oil. The energy index in the Consumer Price Index climbed 0.7% in April, driven by natural gas prices and utilities. Housing inflation also increased over the month, with rent and owners’ equivalent prices moving higher in the month of April.

Fed policymakers have taken a wait-and-see approach when it comes to determining how tariffs and other federal policies will affect the U.S. economy.

Economists reiterated that they believe inflation will follow tariffs in the coming months. We agree with the thought, but it may take a little more time than many first thought. American companies front-ran tariffs by stocking up on products back in February and March. Some tariffs have been suspended for 90 days, and others have been heavily reduced. Overall, we expect to see a slight increase in the annual inflation rate sometime in the summer with further increases to follow.

We do not think this soft inflation report will lead the FED to cut rates (although that is what President Trump wants).

A shorter version of TWB this week. We will be back with a full edition next week. Happy long weekend!

MacNicol & Associates Asset Management

May 16, 2025

Click here for the PDF:

The Weekly Beacon – May 16 2025

{kind=link}

{kind=link}