Morro Lighthouse, Cape Verde

This lighthouse is located on a hill on the east coast of Boa Vista, Cape Verde. The lighthouse was built around 1930 and has a nautical range of 31 nautical miles. The lighthouse is attached to a one bedroom residence for the keeper.

Esaki Lighthouse, Awaji Island, Awaji, Japan

This lighthouse was built in 1871 and is operated by the Japanese National Guard. The lighthouse was originally designed by a British engineer. The Esaki Lighthouse was designated as a National Important Cultural Property in 2022.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Monday morning surprise

On Sunday night, when futures trading began, oil prices continued their ascent, reaching a high of $116 per barrel. Last week, the price of oil jumped by 35%, its biggest futures trading increase since the 1980s.

After Sunday night’s price jump, oil was trading at its highest price since 2022, when Russia invaded Ukraine and the world was still reeling from the pandemic. Many analysts suggested that oil could test record levels this week (in 2008, the price of oil reached $148 a barrel) due to instability and further production disruptions. From a technical standpoint, Brent rising to $200 or even $240 a barrel is “becoming more likely,” Andrew Addison, proprietor of the Institutional View research service, said in a note Sunday. He said a monthly close above $140 would confirm those upside projections. As oil prices moved higher on Sunday night, equity futures plummeted, with many investors worried about the impact of much higher oil prices on companies’ costs and consumer spending.

So why did oil prices surge over the weekend? The continuation of the conflict in Iran has many worried. The conflict seems to be escalating, and both sides are reportedly ready for a prolonged conflict. A prolonged conflict would gravely impact the world’s supply of oil. Iran has also essentially closed the Strait of Hormuz and has threatened to keep it closed if the conflict continues. This will disrupt the global energy supply chain. About 20% of the world’s oil consumption is exported through the Strait. Countries that export oil at risk of further disruptions include Saudi Arabia, the UAE, Iraq, Kuwait, Qatar, and Iran. Due to the Strait’s closure, numerous Middle Eastern nations announced production cuts over the weekend. These production cuts were announced as storage is running out, and crude piles up across the region. Tankers flat out will not travel through the Strait without safety assurances.

Many have speculated that this conflict would need to end, or the U.S. and its allies would need to charter tankers into the Gulf for tankers and insurance companies to resume transports in the region.

Traffic in the Strait of Hormuz has slightly increased in recent days due to Iranian and Chinese linked vessels. However, shipping through the area remains mostly suspended. According to Bloomberg, approximately 13.7 million barrels of Iranian oil have passed through the Strait since February 28th. TankerTrackers told CNBC that Iran has transported a similar number of barrels through the Strait since the conflict began. They believe all of the oil being shipped was destined for China.

Donald Trump posted late on Sunday on social media that these higher prices are a short-term consequence and are “a small price to pay” for Iran’s nuclear threat. The G7 financial ministers met on Monday morning regarding this conflict and the impact it has had on global oil prices. Insiders speculated that a release of strategic oil reserves was being considered in order to combat supply disruptions. Releasing barrels of oil from strategic reserves could cover the gap, but only for a limited period. There are 1.2 billion barrels in the strategic reserves of the 32 members of the IEA. If members released a third of those reserves (double what they released in 2022 when Ukraine was invaded), it would cover the shortfall from the Iranian conflict for only 3-4 weeks. According to reports from Reuters on Monday, around 10:30 am, the G7 decided against releasing strategic reserves and will continue to monitor the situation. However, there were major rumors on Tuesday that Japan, the country with the third-largest strategic reserves, was considering releasing some of its strategic petroleum reserves in order to combat higher oil prices.

On Wednesday, the IEA announced that it would be releasing 400 million barrels of reserves to combat supply shortages. This is the largest oil reserve release in the IEA’s history. The release will be spread over roughly two months. Despite this announcement, global oil prices jumped on Wednesday.

After the massive price spike on Sunday night, prices retreated to $100 per barrel early on Monday morning and to the mid $90s by lunchtime, the low $90s by the afternoon, and back to the $80s by close (oil briefly was trading in the $70s on Tuesday before rebounding; the volatility in energy is astounding this week). The initial oil surge essentially disappeared, which will ease the minds of many consumers and investors. However, oil is still trading nearly $30 higher than it was just a few weeks ago. Prices are higher, and we think they will continue to move this way at least in the short term. Right now, we see neither side backing down, and conditions in the physical market are worsening. Prices slid off their highs on Monday after Trump posted that the conflict was coming to an end and would be a “quick war”. However, a day later, the Iranian regime rebuked these comments.

The one thing we know for sure is that spring 2026 will have higher energy prices across the world. In the GTA, prices have jumped substantially in recent days, and certain economists expect the U.S. national price for gasoline to hit $5/gallon sometime this spring. We believe that if oil and energy prices continue to move higher or remain elevated, the inflation rate across the world will begin to rise once again. A higher inflation rate will lead to no interest rate cuts this year by the FED, BOC, and other Central Banks and will potentially result in contractionary monetary policy to combat rising prices.

Profit taking

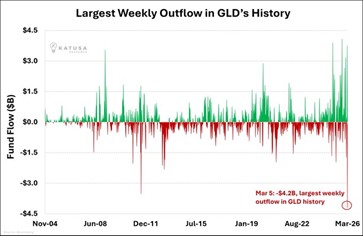

In a tale as old as time, investors have begun taking profits in a highly profitable trade from the last few years. According to Katsua Research, the ETF, GLD (the world’s largest gold-backed ETF), saw its largest weekly outflow in 20 years of history.

The ETF saw $4.2 billion in outflows last week. According to Koyfin, GLD also had its largest daily outflow on Wednesday, March 4th, since November 2016. This follows a record start to the year with global gold ETFs seeing $5.3 billion in inflows in February and $18.7 billion in inflows in January. In February market gold ETFs saw the 9th straight month of inflows. 2026 was also the best two-month start for gold ETF inflows on record.

Previous to last week’s outflow, the largest GLD outflow occurred in 2010 and amounted to $3.5 billion.

We think this trend is natural, especially with the surge in gold and gold miners. When you pair that surge with today’s uncertainty, you get some profit-taking and investors derisking their portfolios. We will also say that as investors flee paper gold ETFs like GLD, Central Banks continue to pile into physical gold as countries push to decrease their U.S. dollar holdings.

Despite gold prices and precious metal miners leveling out in recent weeks, we continue to believe they have more upside and there will be fresh highs sometime this year. We remain in the camp that precious metals, both physical and miners, belong in most investor portfolios (dependent on their risk profile and investment constraints). We believe that these assets provide uncorrelated returns to other asset classes and provide a hedge against uncertainty and a resurgence in inflation.

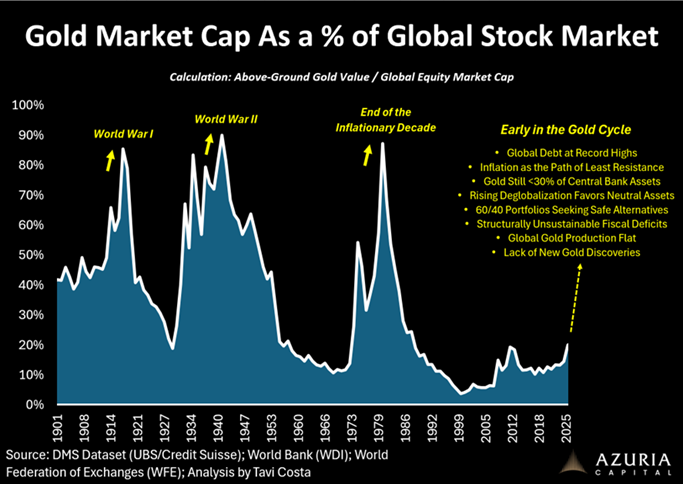

We will also say that, compared to previous gold cycles, gold could still be in the early stages of a bull cycle. Today golds market cap as a percentage of the global stock market capitalization is significantly lower than during previous bull cycles, according to data from Azuria Capital, Tavi Costa, and financial databases:

goEasy goes under

On Tuesday, a well-known Canadian alternative financial services company, goEasy, announced the suspension of its dividend amidst surging loan losses just two weeks before it was due to release its fourth quarter earnings. The company also announced that it would be writing off an additional $233 million in consumer loans, interest, and fees this quarter. According to the firm, many of the firm’s bad loans emerged in its auto lending unit. GoEasy also withdrew its previously released financial guidance and released new guidance that sees mid-teens net charge-offs through the end of 2026 before declining in 2027.

Many had feared this dividend cut would eventually occur, as recent earnings have disappointed investors and have indicated that some troubles are under the hood in the form of bad loans. The bad loans have essentially piled up too high to ignore.

GoEasy also released that its total net charge-offs for the fourth quarter of 2025 were $331 million. The firm also released that it expects to breach covenants and is in ongoing waiver discussions with other lenders.

This news release led to massive selling from investors in goEasy shares. Shares were down 51% as of 11am EST on Tuesday morning. Shares moved another 20% lower on Wednesday morning.

GoEasy was founded in 1990 and has been a darling of Canadian investors for more than a decade and a half. GoEasy shares surged from $6 in 2012 to $216 last September. The company was a great example of a consistent compounder. GoEasy provides customers with subprime loans.

Since then, shares have collapsed by more than 80%. We have been longtime buyers of goEasy shares, but our thesis changed last fall when goEasy reported some troubling results in September. An independent research firm also released a short report against the company (in September 2025), which painted a grim picture for goEasy, stating that the company utilized aggressive accounting policies for years. The short report stated that the firm was inflating earnings, had massive loan losses, and had been delaying charge-offs for quite some time.

We began selling our goEasy holdings in numerous tranches in a tax-efficient and structural way beginning in September. Our final sales came just a few weeks ago. This recent sell-down did not impact us as we were completely out of goEasy above $100/share. We have simply believed the downside has greatly outweighed the short-term upside of holding shares for some time, and believe that to be true today. The company’s loan losses were too big to ignore, and many on the street seemed worried. These fundamental issues, paired with technical weakness, led us to sell a long-time position in goEasy.

Private equity’s golden age behind us?

The Ontario Teachers’ Pension Plan posted its fund results on Tuesday for 2025. The fund printed a 6.7% return for the year, significantly lagging broader public market indices. The OTPP’s benchmark return was 11.7% last year, reflecting major negative value added by the pension plan.

The fund’s private equity assets lagged the most amongst broad asset classes, clipping a return of -5.3%. This was the OTPP’s first negative year in private equity since 2009.

The value of the OTPP’s private equity holdings dropped by approximately $10 billion (CAD) last year. As of year-end, private equity made up 19% of the fund’s assets. According to leadership at the fund, year-end valuation adjustments weighed on performance.

These negative private equity returns led to the pension fund restructuring its private equity investment management team.

Institutional investors have reaped the rewards of private equity investing for well over a decade. That tune seems to be coming to an end as exit opportunities disappear, valuations contract, and funds struggle to raise assets for private market funds.

The pension’s real estate portfolio also realized a negative return in 2025, driven by negative returns in the domestic market. Domestic retail real estate, driven by Hudson Bay’s insolvency, and office real estate saw decreases last year in the OTPP’s portfolio.

The fund’s strongest performing assets last year included venture growth, gold, and public equities. On a positive front in private markets, the OTPP has an investment in SpaceX and participated in a raise for Anthropic last year.

The fund posted a C$1.2 billion loss from foreign currency exposure, mostly due to the U.S. dollar’s slump.

Beyond some trouble in private equity from an allocator’s perspective, private credit is also still seeing issues. These issues are being driven by limited exit opportunities, decreased liquidity, and companies’ cash flows shrinking due to AI.

This week, JPMorgan reportedly will begin limiting its private credit lending to funds after marking down the value of certain loans in its portfolio. Most of the devalued loans they have marked down are from software companies, a sector that has been hit very hard in recent months due to investor concern over the potential impact of AI. According to private credit executives, other banks have not taken the same view as JPMorgan as of now.

It’s tough sledding in private markets, no matter whether you are in equity or credit.

Chart of the week

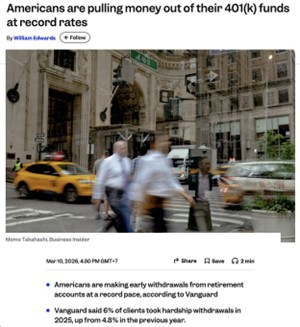

Consumers are really feeling a breakdown in economic conditions. The lower and middle class has seen their financial balance sheets deteriorate in recent quarters. This has led many Americans to pull money out of their investment accounts to service the shortfall in their expenses.

A breakdown in economic conditions is being ignored by many. What happens when balance sheets continue to deteriorate? Consumers will be forced to make tough decisions and will avoid discretionary items. We hope your portfolio is positioned appropriately.

What we are looking at next week:

Markets will enter the week of March 16th with volatility front and centre after the CBOE Volatility Index spiked to 35 earlier this week — its highest level since the tariff-driven market shock nearly a year ago. The surge reflected a rapid repricing of risk as investors reacted to renewed uncertainty across policy, geopolitics, and global growth expectations. Since that spike, however, volatility has moderated meaningfully, with the VIX falling back below 25 as markets stabilized later last week (as of Wednesday, March 11). The key question heading into next week is whether this cooling trend continues or whether the recent decline in volatility simply represents a temporary pause within a broader period of market turbulence. Historically, volatility spikes of this magnitude are rarely resolved in a single move; they often give way to several weeks of uneven trading as investors reassess positioning and risk exposure. This is especially true with markets at their current, elevated valuations.

As a result, the focus for investors next week will not necessarily be on a single economic release or policy event, but rather on whether markets can sustain this stabilization in volatility. If the VIX continues to trend lower, it would suggest that the initial shock has largely been absorbed and risk appetite is gradually returning. If volatility begins to climb again, it would signal that markets are still in the process of digesting recent developments and that the period of choppy, headline-driven trading may not yet be over.

March 13, 2026

MacNicol & Associates Asset Management

Download in PDF format: