Chania Lighthouse, Chania, Greece

This lighthouse is located on the southern island of Crete. The current lighthouse was built in 1864 and was built to protect Crete. The lighthouse suffered damage in World War 2 and was refurbished in 2006.

Patras Lighthouse, Agios Andreas, Patras

This lighthouse is a landmark in Greece and is situated opposite the temple of Saint Andrew. The lighthouse was originally constructed in 1880 and the current lighthouse was first lit in 1999.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Private credit

Over the past few months, we have discussed private markets in depth. For this commentary, which is rare, we usually stick to public markets. However, at our firm, private markets are nothing new. We have been private market investors for closing in on two decades. Investors with us gain exposure to private markets through the Alternative Asset Trust, a Trust that offers access to these markets. The Trust invests in private equity, North American private real estate, and hedge funds. We have built a very diverse investment vehicle that we think complements investors’ public market assets. For the most part, we have avoided other asset classes like infrastructure and private credit.

Despite avoiding these specific asset classes, we are watching them very closely. In recent months, there has been major news regarding private credit. We have outlined those issues and the state of private credit markets in depth in this publication. We will not bore you by repeating ourselves this week. If you do not know what we are talking about, read our recent commentaries and skip to the entries on private credit.

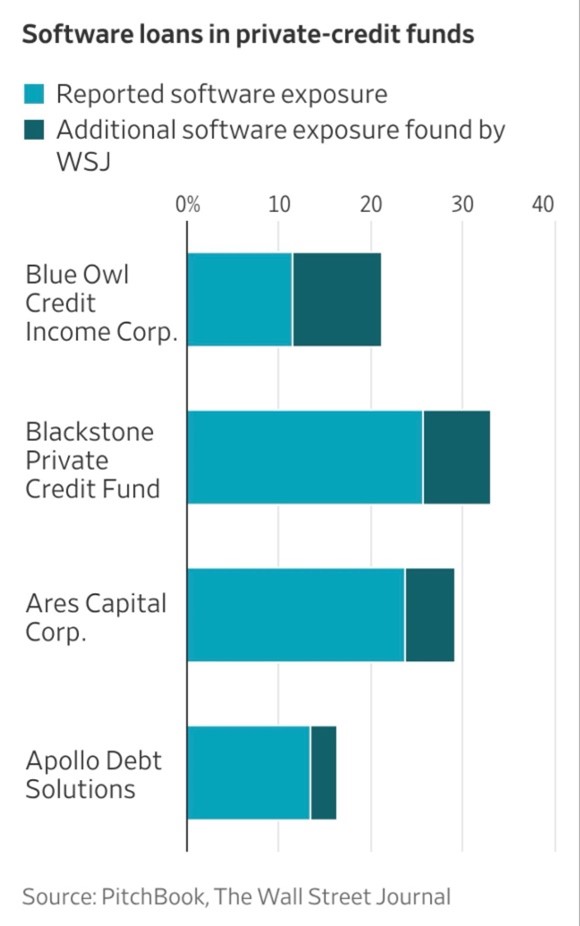

We bring this up this week because of an article that the Wall Street Journal released on Sunday that we read. The article titled “Private Credit’s Exposure to Ailing Software Industry is Bigger Than Advertised” outlines how fund managers at private market asset managers are underreporting their exposure to software in their filings. The report looks at four mega funds, the private credit funds of Blue Owl, Blackstone, Are Capital, and Apollo. They are four of the largest private market asset managers, and all four have been in the news recently due to the gating or suspension of redemptions in their respective funds.

So why is underreporting software exposure a smart move, although unethical for these asset managers? Private credit and equity have heavily invested in software over the last decade plus. Those investments delivered strong returns for years; however, that has changed with AI. Many fear AI will disrupt the software space and make many of these software firms obsolete. This would impair loans and potentially destroy investment capital. These software fears are a primary driver of investors’ redemption requests in recent months.

Getting into the article, according to the Wall Street Journal, Blue Owl’s fund has nearly doubled the amount of software exposure as reported. On average, the four funds classified 19% of their investments as software, but analysis reveals that, on average, more than 25% of their assets are software. Industry classification varies by firm as they use different data sets or classification systems. According to a Barclays analyst, this “sector massaging” is a great concern as it makes it difficult to assess diversification across a fund.

So, what is “sector massaging”? Private credit funds can invest in a healthcare-based software firm and label it as a healthcare company in its databases. This massaging makes their portfolios look more diverse than they really are. According to The Wall Street Journal, Blue Owl categorized loans to 47 software companies in other industries, ranging from transportation to education. Blackstone categorized over $1 billion of loans to Inovalon as IT Services. Inovalon’s website states that it’s a software company that empowers healthcare organizations. One of Ares largest loans is to Symplr Software, a SaaS firm which Ares classified as a health care equipment services firm. The report went as far as to say that these mega-funds even classified the same firm into different industries. Our assumption is that they classify assets as they see fit and what serves them best. Right now, nothing in software serves them best.

The Wall Street Journal also found that the funds that have grown the fastest have more assets classified under different industries. Some investors worry that this rapid growth will severely hurt the quality of the loan portfolios. Right now, private credit is shrinking, investors are trying to redeem, banks are decreasing their exposure, and exit opportunities are few and far between. Buckle up, this could get uglier.

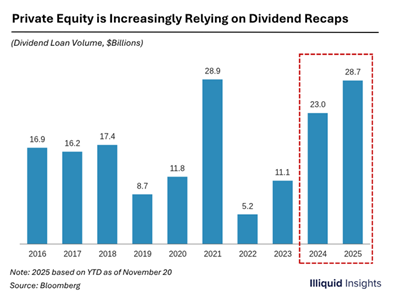

A major problem for private credit stems from private equity. Private credit often invests alongside private equity. The issue today is that private equity holding periods have increased recently due to a slowdown in exits. These funds are sitting on companies longer than ever before. These private equity funds are now relying on dividend recaps to fund distributions.

Record month

Oil prices moved even higher on Monday, even as President Trump posted that his administration was having “serious discussions” about ending its military operations in Iran. As of mid-day on Monday (March 30th), oil prices were on track for one of their largest monthly gains on record.

Oil prices pushed higher on Monday as the Strait of Hormuz remains closed. Events over the weekend that pushed prices higher included Iranian allies, Yemen’s Houthi rebels entering the conflict, as well as a report from The Wall Street Journal that stated Trump was considering a military operation to extract uranium from Iran. West Texas Intermediate future prices have increased by more than 50% this month, the largest gain since May 2020. Deutsche Bank’s strategist stated that investors are beginning to price in higher oil prices for an extended period, which would bring on stagflationary pressures for the global economy. Traders are reportedly beginning to price the risk of U.S. troops being on the ground in Iran, which would certainly accelerate this conflict. Ed Mills, Washington policy analyst for Raymond James, wrote in a note on Friday that they view the risk of escalation as “more likely than not, even with a renewed diplomatic effort underway.”

At an energy conference in Houston this week, the executives of numerous oil companies stated that the market is underpricing the potential impacts of the lost supply (from this conflict). The Chevron CEO stated that the market is in a supply shortfall of about 11 to 12 million barrels per day, and the price today reflects a resolution to this conflict tomorrow, not down the line.

We will warn our readers that we wrote this piece before President Trump gave his address to the nation on Wednesday night. According to statements from Trump and insiders, an end to the war will be announced. These thoughts sent markets higher on Wednesday. Despite optimism regarding an end to the conflict in Iran, oil prices continued to trade near $100/barrel midday on Wednesday.

We think Trump is attempting to end this war arguably before it starts due to a lack of support from his base. The conflict has sent oil prices higher, which has reignited inflation worries. Trump has also been anti-war and promised his supporters he would bring peace to the world and no new conflicts before the last election.

Evergrande situation

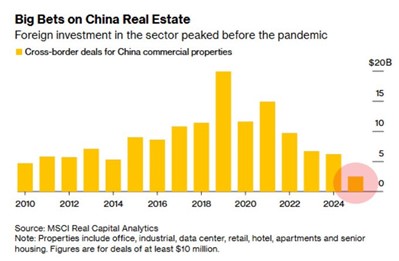

The Chinese property downturn that has unfolded in front of our eyes over the last five years can best be described by the situation Evergrande went through a few years ago. For those of you unfamiliar with Evergrande, it was a real estate giant in China that was delisted last year and liquidated after building a debt-fueled business model that required constant new borrowing and strong home sales. At its peak, the firm was the most indebted property developer in the world. Things collapsed when the Chinese property market slowed down, and credit conditions changed. Many developers across China faced similar issues as Evergrande, where they became highly distressed, and defaults surged.

We bring this up because the Chinese real estate market remains weak, and foreign investment is nowhere to be seen. Last year, China saw its lowest foreign investment in real estate since the financial crisis. Foreign investment has decreased by more than 80% since 2019, according to data compiled by Bloomberg from MSCI Real Capital Analytics.

Foreign investors have shifted capital away from China as a whole based on policy and risk. When you pair the general risk that China exhibits with the financial distress and economic trends in the real estate market, many foreigners sell and do not look back. Essentially, the Chinese real estate market, which had seen strong growth for years, became uninvestable over a few short years for many investors.

We have, for the most part, avoided China completely due to the risks associated with buying in their market. The only exposure our clients have to China is some indirect exposure through the iShares Emerging Markets ETF.

Disclaimer: MacNicol & Associates Asset Management Inc. holds shares of EEM across several client accounts.

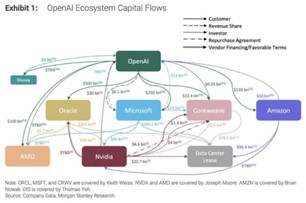

AI and circularity continues

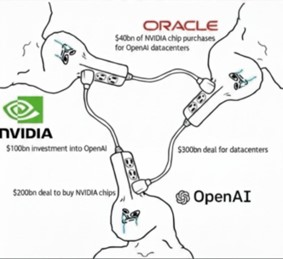

For close to a year now, we, along with many other investors, have been warning our readers regarding the risks associated with the AI trade. Beyond stretched valuations, slow adoption, and delayed revenue, investors in the space are exposed to circularity. What do we mean by circularity? Circularity in the AI ecosystem refers to financing and supply chain deals in the industry that seem to follow a circular trend (we have talked about this over the last 6+ months in this publication).

This trend has led to hyperscalers like Microsoft, Amazon, and Alphabet, chipmakers like Nvidia, AMD, and AI developers like OpenAI, Perplexity, and Anthropic making deals to supply each other, invest in each other, and sign exclusive rights deals. The issue with this trend can be explained by a few pictures that we have shared over time:

The two images above are slightly out of date. Over the last month, Morgan Stanley updated it, and the industry is even more complex and CIRCULAR today.

We think this circularity is a huge risk. What happens when the tap turns off, and investment in the space slows down, which decreases orders. The market is heavily reliant on strong numbers from the megacaps like Nvidia, Microsoft, and Alphabet. OpenAI and many AI companies are producing low revenues and are financing their chip and computing capacity purchases through investment, much of which is coming from the same companies they are buying chips and computing capacity from.

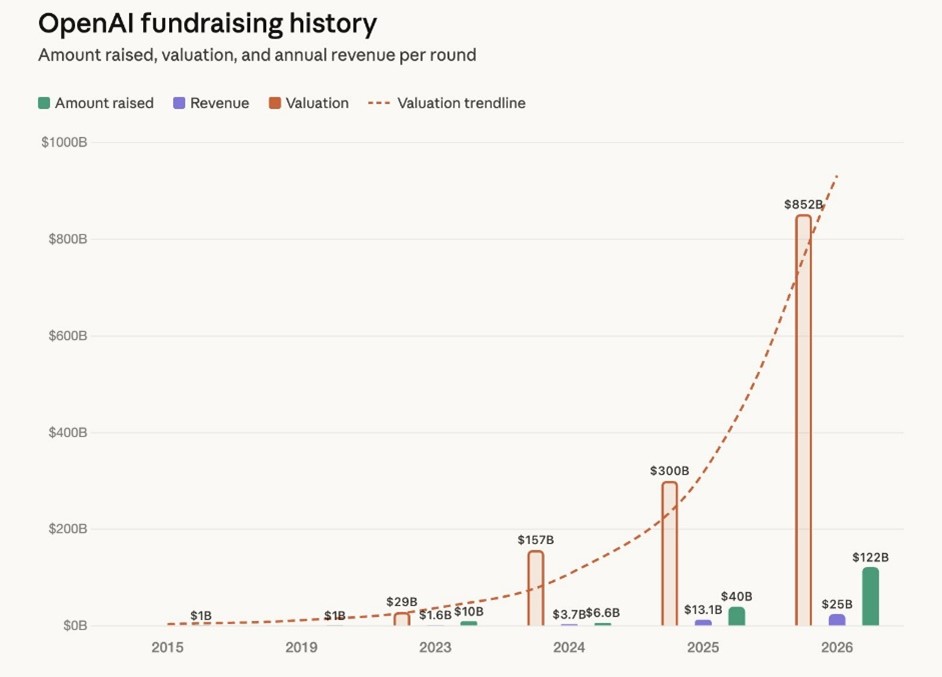

We bring this all up this week because OpenAI announced on Wednesday that it received $122 billion in new funding. The company also stated that it is elevating its valuation to $852 billion ahead of a potential IPO later this year. This new valuation makes OpenAI one of the world’s most valuable private companies and is much higher than its last raise from 2025:

The funding includes a $50 billion commitment from Amazon. This diversifies OpenAI’s hardware and cloud resources away from Microsoft. OpenAI has historically utilized Microsoft’s cloud computing and hardware. Amazon’s commitment of $50 billion is structured with a $15 billion investment, followed by a $35 billion tranche contingent on certain milestones. OpenAI signed a $100 billion deal with Amazon Web Services after Amazon made its financial commitment. SoftBank and Nvidia also made $30 billion commitments, and Microsoft also participated in the round. On the individual and fund front, Cathie Wood’s Ark Invest participated in this raise through Ark’s managed ETFs.

On Tuesday, OpenAI stated that it is now generating $2 billion in monthly revenue and expects to soon reach one billion active weekly users. However, margins have shrunk for OpenAI in recent years as costs have surged. Despite OpenAI’s recent growth rate in terms of revenue and users, the company continues to burn cash monthly. Cumulative losses are expected to hit $115 billion through 2029, and the firm expects to spend $600 billion on compute by 2030.

According to internal projections, the funding received could run out in 18 months. The $122 billion raise will reportedly finance 18 months of runway when paired with OpenAI’s current run rate and pending projects. The raise is not pure cash for OpenAI, as some of the investment is tied to product credits (Nvidia) and milestones (Amazon). Investors could face further dilution even after an IPO due to capital requirements.

Endless capital raising, massive investment from the same companies over and over, and now Cathie Wood. The OpenAI story is littered with risk from an investment perspective. ETFs buying private companies is nothing new, but it does present a new risk for retail investors who may not understand the liquidity constraints of private market investments.

We will be clear, we are not questioning the application or innovation of AI, we are questioning the circularity funding and growing it. We think investors should understand and be more mindful of these risks, especially in today’s elevated markets.

goeasy reports

Canadian subprime lender goeasy has been in the news over the last 6-8 months for all the wrong reasons. Leadership changes, massive loan losses, credit issues, charge-offs on investments, and delayed earnings. These news pieces have led shares to draw down by more than 70% over the last year.

We were long-time holders of goeasy and liked the business model for years. However, that changed over the last year. We slowly began selling last fall when the company reported weak earnings, higher loan losses, and announced a leadership shuffle. We closed our position due to tax reasons in the new year, just a few days into 2026. We are glad we sold and remained disciplined as shares have cratered since.

On Tuesday night, the company finally filed its fourth-quarter earnings, and shares pulled back another 10% despite markets having a strong day. This is because goeasy reported a quarterly loss due to an investment in LendCare. Charge-offs surged from 9.2% to 23.8% year-over-year. The firm missed most revenue and earnings forecasts. The firm guided charge-offs up to 13% just two weeks ago but revised that this week to 18% for the year. For a benchmark, the normal level is only 9%.

This earnings release confirmed two things for us: one, goeasy stock remains a no-go for the foreseeable future, and two, Canadian consumers are hurting more than headlines would suggest. Buckle up.

What we are looking at next week

After markets staged a sharp rally this week, investor focus now turns to next week’s CPI release, where the key question will be whether the recent spike in oil prices begins to filter into headline inflation. The Iran conflict has already pushed crude above $100 at points and disrupted a meaningful portion of global supply, and early estimates suggest this is starting to lift headline inflation even as core measures remain more stable. Investors will be watching closely to see whether this remains a temporary energy-driven bump, or the beginning of a more persistent inflationary impulse.

The distinction between headline and core inflation will be critical, as markets assess whether central banks are forced to respond. If CPI shows a clear pass-through from higher energy costs, it would reinforce concerns that inflation is re-accelerating, particularly given how sensitive expectations have become to oil shocks. At the same time, there is still a competing narrative that these effects may prove transitory, meaning next week’s data will play a central role in determining whether this week’s rebound can extend, or whether inflation concerns quickly reassert themselves. Any upside surprise in inflation would likely reintroduce pressure on equity markets by pushing rate expectations higher and tightening financial conditions just as sentiment has begun to recover.

April 3, 2026

MacNicol & Associates Asset Management

Download in PDF format:

{kind=link}

{kind=link}