Bari Light, Bari, Italy

This coastal lighthouse is located off the east coast of Italy on the Adriatic Sea. The lighthouse was originally built in 1869 and stands at 62 meters high. The lighthouse is the 24th tallest traditional lighthouse in the world.

Roches-Douvres Light, Côtes-d’Armor, France

This active lighthouse was originally built in 1868. The lighthouse is the 11th tallest traditional lighthouse in the world and sits on an island only accessible by boat off the coast of France.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Trump hits a sector

President Trump is infamous for making rash and unanticipated announcements online and at press conferences. His comments or policy stances often lead to big moves in financial markets. Last Friday, Trump posted on Truth Social that he will cap credit card rates in the U.S. at 10% for one-year, effective January 20th.

Trump is attempting to improve affordability for Americans, and this policy decision is the latest attempt to fulfill that goal. However, do not expect the interest rate on your credit card to change overnight, as, according to Raymond James, Trump does not have this authority; it would require an act of Congress. According to a Jeffries analyst, a Bill of this nature would be dead on arrival in Congress. Truist analyst Brian Foran said this move would make credit card providers unprofitable in their credit card business segments.

Despite no official change to credit card interest rates and the likelihood of a Bill being passed being extremely low, financial stocks moved lower on Monday, led by credit card providers like American Express and Capital One. Large U.S. banks with credit card exposure also moved lower.

Trump’s surprise announcement regarding credit card interest rates came just days before, and most Wall Street firms are set to deliver fourth-quarter earnings, beginning with J.P. Morgan Chase on Tuesday. His announcement regarding credit card interest rates has been critiqued by most banks, including Wells Fargo’s CEO, who stated that this move would hinder the ability of some Americans to access credit and negatively impact affordability. The proposal, if put into effect, could slow consumer spending and force companies to weaken credit card reward programs to compensate for lost revenue. It may also spur lower-income customers to turn to buy-now-pay-later companies and personal loan providers.

On the earnings front for Wall Street, we are watching several numbers despite not having major exposure to any Wall Street firm. Beyond the forecast of earnings and revenue for each business unit, we will be paying attention to U.S. bank targets for returns on tangible common equity. This ratio is its return on equity with preferred stock, intangibles, and deferred tax assets excluded. This ratio can spark financial stocks beyond quarterly earnings beat. Analysts pay close attention to this ratio as it isolates profit generated by loss-absorbing tangible capital base, which ultimately protects creditors and helps drive long-term shareholder value (and returns). Banking by nature is a leveraged industry where regulatory capital and tangible common equity determine risk appetite and assets the bank can carry. Return on tangible common equity illustrates how efficiently that capital is being utilized. Banks with higher returns on tangible common equity often trade at higher multiples.

On Tuesday, J.P. Morgan Chase reported earnings before the bell, and shares moved lower after the company missed headline earnings estimates and reported lower profit than last year. J.P. Morgan shares have been suffering the effects of Trump’s credit card interest rate cap as they dive further into the credit card industry.

J.P. Morgan’s fourth quarter profit dropped by 7% year-over-year to $4.63/share, but adjusted earnings topped street estimates. J.P. Morgan’s profit came in lower than expected during the quarter due to the financial impact of a new deal with Apple regarding the Apple credit card. J.P. Morgan realized a $2.2 billion pretax charge for a credit reserve established for the forward purchase commitment of the Apple credit card portfolio. When the Apple credit card credit reserve was removed from J.P. Morgan’s results, the company reported earnings-per-share of $5.23. A major driver of adjusted earnings growth was trading volume. Its core Wall Street revenues from equities, fixed income, currency, and commodity trading rose 15% from the fourth quarter of 2024, ahead of analyst expectations. Investment banking fees fell by 5% in the quarter as deal activity slowed at the end of 2025. Analysts, for the most part, were impressed with J.P. Morgan’s results aside from the credit exclusion related to the impact of the Apple deal.

Revenue rose 7% YoY, and net interest income rose 7% to $25.1 billion. The company’s revenue came to 1.1% above street expectations. Net income for J.P. Morgan Chase slipped by $1.5 billion in 2025 versus 2024. J.P. Morgan Chase CEO Jamie Dimon mentioned the resilience of American consumer spending as a driver of the firm’s strong numbers. He also stated that although the labor market is soft, they do not see conditions worsening.

J.P. Morgan Chase returned significant capital to shareholders during the quarter, including $4.1 billion in common share dividends and $7.9 in net stock repurchases. These returns of capital to shareholders come at a time when J.P. Morgan shares are trading at all-time highs after a very strong year for the firm.

J.P. Morgan’s return on tangible common equity came in at 18%, down slightly from the fourth quarter of last year but remaining in a strong position, supported by strong fee franchises and balance sheet strength. The firm reiterated its target for the ratio of high teens.

The bank projects slightly better net interest income than expected and higher expenses in 2026, driven by technology, regulatory, and growth requirements.

J.P. Morgan Chase earnings give investors their first look at how banks held up in the fourth quarter. J.P. Morgan Chase shares were up 34% last year. Later in the week, Citigroup, Wells Fargo, and Bank of America reported earnings; all three firms beat adjusted earnings estimates, and Wells Fargo and Citigroup slightly missed quarterly revenue estimates.

Overall, the quarter seemed strong for Wall Street, results did not jump off the page to beat estimates. To be frank, investors expected more. All firms reported strong wealth management numbers driven by more assets.

Disclaimer: MacNicol & Associates holds shares of select Wall Street banks across select client accounts.

Powell vs. Trump

This past week, the latest saga between President Trump and Federal Reserve Chairman Jerome Powell unfolded and it looks to be getting nasty and personal. The Department of Justice is currently investigating Chairman Powell regarding a renovation of the FED’s Washington headquarters. The DOJ issued a grand jury subpoena to the FED and threatened an indictment tied to Chairman Powell’s testimony in the Senate last June.

Powell called the move political and part of Trump’s pattern to pressure him and the FED to lower interest rates.

Trump spoke with reporters on Tuesday and called Powell either “crooked” or “incompetent” regarding the FED’s multibillion-dollar renovations. According to sources, the renovations have gone way over budget ($700 MM US by some measures), and the President has even floated suing Powell personally (according to legal experts, this faces numerous hurdles).

There has been bipartisan opposition to this move from Trump and his allies. Senator John Kennedy, a Republican lawmaker from Louisiana, stated, “If you wanted to design a system to guarantee that interest rates would go up and not down, the best way to do that would be to have the Federal Reserve and the Executive Branch of the United States get in a pissing contest.”

This is the latest move by the President to push Powell out as the FED’s Chairman or convince him to fall in line and conduct monetary policy as Trump wants. Remember, the FED is designed to be an independent institution. Trump is attempting to remove that independence and push the FED to slash rates at a faster rate than they have. Trump wants lower interest rates to stimulate economic activity and continue the boom in financial markets. Powell and the FED have a dual mandate to balance inflation with the jobs market.

J.P. Morgan Chase’s CEO Jamie Dimon stated that this move by Trump and the DOJ could impact the FED’s independence and undermine the public’s confidence in the Central Bank. Dimon went on to say that eroding confidence in the FED will raise inflation and, more than likely, raise interest rates over time. Dimon was careful with his words when talking about the FED, stating that he does not agree with all its policies, but added that he has enormous respect for Jerome Powell.

Treasury Secretary Scott Bessent expressed concerns to Trump over this DOJ investigation, stating that it will complicate plans to confirm the next FED Chairman in the Senate when Powell’s term expires in May.

Regardless of how you feel about monetary policy in the U.S. right now and Jerome Powell, this seems very short-sighted and highly risky for Trump and the DOJ. Why not just wait five more months and nominate your guy?

Inflation update

The Bureau of Labor Statistics released the consumer price index for December on Tuesday. The CPI report comes during a very busy week where numerous government statistics will be released, Wall Street reports earnings, and as Trump spars with Powell.

The latest inflation report came in at 2.7% for 2025, which matched November’s pace. On a monthly basis, inflation ticked up by 0.3% in December. Inflation finished down from the 2025 high of 3%, experienced in September, but well above the FED’s target of 2%. Inflation has remained above the FED’s target for more than four and a half years. Core services inflation remains above 3%. One of the bigger gains in the services category was in airfare prices, which rose 5.2% month over month in December. Housing inflation rebounded in December, increasing 0.4% in December, a notable increase from the 0.2% increase seen from September to November. Energy costs have been falling, which has assisted in keeping headline inflation low; however, in December, the index for energy jumped by 0.3%, driven by natural gas prices jumping 4.4%.

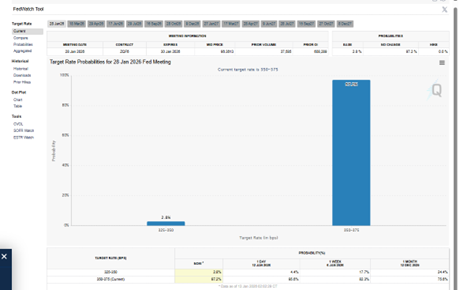

This inflation report will be a major data point that the FED uses at its January Policy decision at the end of the month. According to the FED Watch Tool from the CME Group, there is a 97.2% probability that the FED funds rate stays the same at January’s meeting. This probability implies a 2.8% probability of an interest rate cut; one month ago, the probability was 24.4%. LPL Financials’ Chief Economist stated that monthly inflation increases will need to reach 0.1% and 0.2% (versus 0.3% in December) before investors and the FED can conclude that inflation is under control.

Trump used Tuesday’s inflation report as his latest reason to call on the FED and Chairman Powell to cut rates, stating if they do not, “it will be too late”.

China trade report

China reported its 2025 trade data this past week and reported its largest-ever trade surplus last year. China’s trade surplus reportedly reached $1.2 trillion last year, increasing 20% from 2024 despite the implementation of tariffs by President Trump. Last year, China’s monthly trade surplus exceeded $100 billion seven times. This trade surplus was supported by a weaker Yuan. China’s foreign trade hit a new record last year of $6.35 trillion.

Source: Financial Times

Chinese exports to the U.S. decreased by 20% in dollar terms last year, while imports from the U.S. decreased 14.6%, highlighting the impact of tariffs and tensions boiling between the world’s two largest economies. China made up for American losses by increasing its exports to emerging markets across Africa (25.8% increase) and ASEAN countries (13.4% increase). Chinese exports to the European Union also increased last year by 8.4%, and its trade surplus with the bloc hit an all-time high by 18.1%. This trade surplus with the EU was driven by tariffs and the U.S. decreasing its reliance on China. Now, China is flooding developed European nations with its goods. China is taking advantage of the EU’s open markets and is fully entrenching itself in numerous critical sectors across the EU, including EVs, batteries, and solar panels.

We do not expect a reversal in policy by the U.S. over the next few years. We think a major focus for the Americans will be to decrease or eliminate their reliance on China in critical sectors. For now, this will be offset by European demand; however, many European nations could create a major issue for themselves down the line by boosting their reliance on China. What happens when geopolitical tensions rise, and China cuts off exports of something?

China’s exports grew by 6.1% last year, and its imports rose by 0.5%. In December, Chinese exports jumped by 6.6% year-over-year; economists had expected a 3% increase. According to Pinpoint Asset Management, a strong export market mitigated domestic consumer weakness in China.

Chinese rare earth metal exports surged to their highest level in a decade, even as Beijing sanctioned and curbed some shipments. China also benefited from the increased global demand for computer chips.

Pinpoint Asset Management pointed to stability between China and the U.S. at the end of the year, and a strong export market as reasons for the Chinese Central Bank to keep its macro policy stance unchanged to begin 2026. In other words, do not expect another massive Chinese stimulus package from the Chinese in the short term. Economists expect exports to remain strong for China in 2026 and will be a big driver of growth. Gary Ng, a senior economist at French investment bank Natixis, forecasts that China’s exports will grow about 3% in 2026, less than the growth in 2025.

Chinese equity markets have rebounded nicely since their April 2025 bottoms and remain cheap. However, we still think there are major risks in purchasing Chinese equities or assets that hold Chinese equities. We have looked to other emerging markets that are growing rapidly for non-developed global exposure, including India, and in Latin America.

We think these markets offer cleaner growth stories, improving policy environments, and are safer in terms of geopolitical and regulatory risk versus China. India’s domestic demand, infrastructure, and per capita growth have grown in recent years, helping justify strong forward earnings growth (brokers forecast EPS in India to increase by 15% in 2026). Numerous Latin American countries are expected to outgrow developed nations in 2026 as capital returns, political landscapes improve, and countries/companies diversify supply chains. These countries also have highly attractive valuations in their equity markets and could see some explosive returns as their financial markets advance.

Disclaimer: MacNicol & Associates holds shares of ETFs and Trust Companies that buy emerging market equities, including but not limited to India and Latin America.

MacNicol & Associates Asset Management

January 16th, 2026

What We Are Looking At Next Week

Next week world leaders will converge on Davos for the World Economic Forum Annual Meeting (Jan 19-23). Davos matters less for formal policy announcements and more for signaling: coordinated language, shifts in tone, and off-script remarks all can trigger market reactions. With growth concerns, inflation persistence, and geopolitical fragmentation all coming to the fore, markets will be listening for alignment–or lack thereof–between political leaders, central banks, and corporate executives.

Given the events of the last few weeks, a central theme at Davos will likely be geopolitical and economic uncertainty. The recent U.S. intervention and arrest of Venezuelan President Nicolas Maduro in Caracas have significantly elevated geopolitical risk, and discussion will likely be vigorous on whether such actions foreshadow broader U.S. military engagements or shifts in foreign policy. If this doesn’t register as historically high geopolitical uncertainty, just look to gold and silver which have both made new all-time highs amid historical safe haven demand. The first large scale assembly of global leaders at Davos will provide a forum to consolidate what has been happening lately and likely set the tone for the coming months.

Intertwined with these political threads is Donald Trump’s posture towards both geopolitics and monetary policy, particularly the U.S. Federal Reserve. His ongoing public pressure on the Fed and criticism of rate policy raises questions about central bank independence, especially as Jerome Powell’s tenure comes to a close and with ongoing DOJ scrutiny, which many see as being politically motivated to pressure the bank. A strong, unified defense of monetary independence would likely support higher real yields and restrain risk assets, but ambiguity on the topic at Davos would likely do the opposite. In short, next week is about narrative formation, not data–and those narratives will set the tone for the first quarter of 2026, if not longer.

Download in PDF format:

{kind=link}

{kind=link}