Boston Light, Little Brewster Island, Massachusetts

This lighthouse was built in 1783 but the light station was established in 1716 making it the oldest light station in the U.S. The lighthouse was designated a National Historic Landmark in 1964. The original tower was blown up by British forces in 1776.

Gillette Stadium Lighthouse, Massachusetts

In honour of U.S. Thanksgiving, we wanted to highlight a modern lighthouse that ties into football. This lighthouse is part of Gillette Stadium, home of the New England Patriots. The “lighthouse” has a 360 degree observation deck and is home to visitors daily.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

U.S. Thanksgiving

We wanted to wish our readers south of the border a happy Thanksgiving weekend and a wonderful holiday season. Enjoy the company, food, and football.

Trump, Xi, and trade

According to the Chinese government, President Trump and Xi held a phone call over the last few days, during which they discussed a trade truce, Ukraine, and Taiwan. According to the Chinese embassy, the two leaders are working to implement all elements of the deal agreed upon during their meeting in South Korea just a few weeks ago.

China stated the importance that Taiwan represents to the country’s post-war international order. A few weeks back, Trump stated that the two leaders never discussed Taiwan while in South Korea. Taiwan is a democracy off the coast of China that has become a major tripwire in the U.S. – China relationship. Taiwan has become westernized in recent decades, but according to China is part of their land. There is growing worry that China could use force to take over Taiwan and reunify the nation over the next few years. Taiwan’s President has rejected this Chinese claim and said the people of Taiwan should have a say in their future.

This worry is a major risk factor that we are monitoring. Force from China could be met with resistance from the West and a direct conflict. Japan’s new leader stated last month that a Chinese attack on Taiwan could trigger a military response from Tokyo. Beijing-Tokyo relations have plunged to a new low in recent months as the two countries spar on a variety of issues. The same could be said for the U.S., which might be forced to respond if China attacks an open democracy. There are also major financial implications at stake as a conflict could grind trade to a halt, trigger more tariffs, and severely impact global economic growth. Taiwan has also become a major hotbed for technological innovation and semiconductor chip manufacturing, which could severely stunt the growth of AI and tech. A conflict at this scale could be a potential black swan event that could trigger a financial meltdown. We are watching it closely.

Taiwan has major ties in the AI industry, as one of the country’s largest companies, Taiwan Semiconductor Manufacturing, produces 90% of advanced chips and manufactures many of its chips domestically.

Trump has maintained strategic ambiguity about whether he would send troops to Taiwan in a war. However, his administration has been urging Taiwan to increase its defense budget. Earlier this month, the U.S. approved $330 million in arms sales to Taiwan, something Beijing has protested greatly.

On the Ukraine front, the Chinese embassy reiterated its support for peace while calling on both Russia and Ukraine to narrow their differences. President Trump also announced big progress in peace talks with Ukraine for a proposal to Russia on Monday. This statement from Trump comes a day after the White House stated that recent talks with Ukraine in Geneva have been constructive and the two sides continue to modify the peace framework. Defense stocks and oil pulled back on Monday after Trump’s statement. We do not think oil will go much lower than where it trades right now. On the defense side, we continue to like a few names and continue to believe that countries and governments will continue to increase their spending on defense. Many of these companies remain highly attractive in our eyes despite the run that they have already gone on this year.

Strategy deep dive

Over the years, we have written a few times about Strategy Inc. (formerly MicroStrategy), a Nasdaq-listed technology firm that provides business intelligence and mobile software. The company is run by Michael Saylor, who also founded the firm in the late 1980s. Saylor has risen to prominence in recent years due to his support for Bitcoin. He has become one of the world’s biggest and loudest Bitcoin bulls. He has turned his company into a Bitcoin derivative through the issuance of preferred shares, bonds, and common shares. Saylor’s thesis for Bitcoin is simple: he believes Bitcoin is the world’s premier store of value, and that it is digital gold. He thinks holding Bitcoin will give Strategy a strategic advantage as they hedge against monetary debasement.

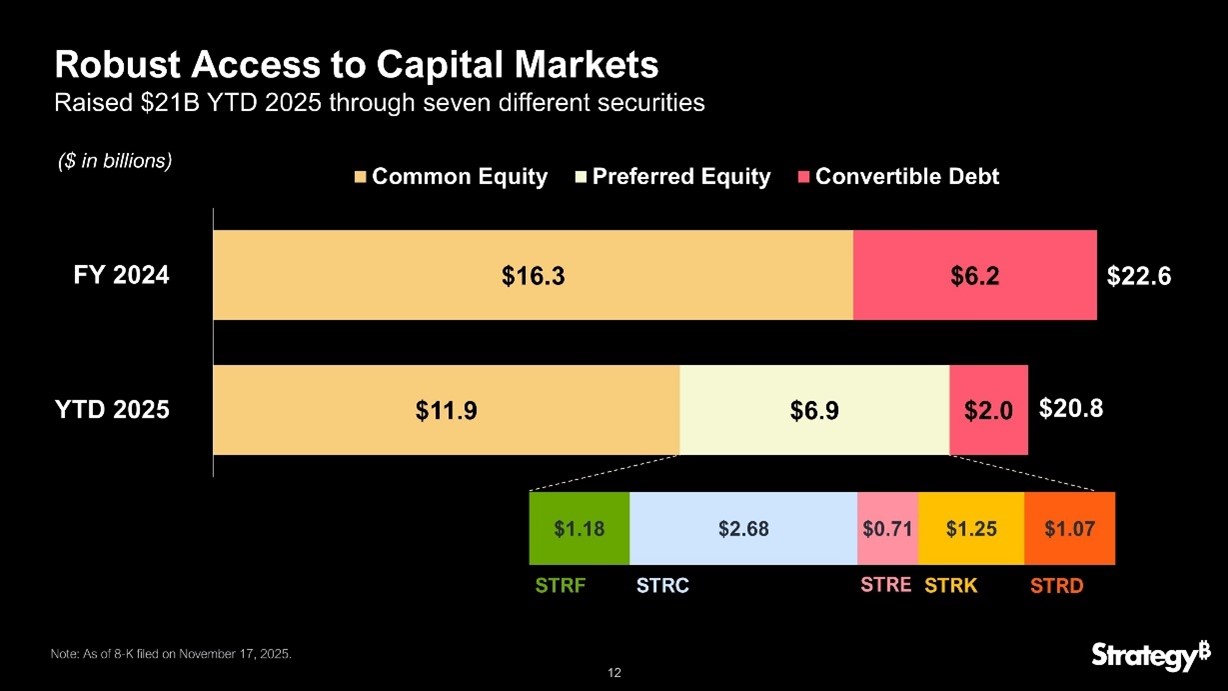

Back in 2020, Saylor began buying Bitcoin on Strategy’s balance sheet. His purchases began small but have ballooned since. Strategy now owns 650,000 bitcoins worth over $50 billion. Strategy currently owns almost 3% of Bitcoin’s supply and has become one of Bitcoin’s largest holders. He turned his software company into a Bitcoin conduit. Many compare his firm to a leveraged Bitcoin ETF due to the company’s performance and strategy. The company has not built its Bitcoin reserves through operating cash flows; the company has issued billions in capital in recent years in order to buy Bitcoin. Here is a snapshot of the amount raised over the last 23 months:

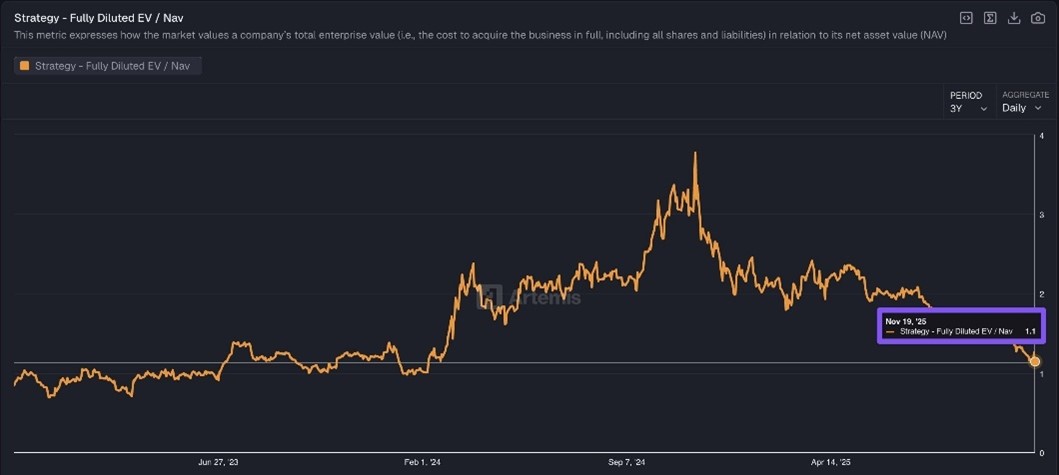

Strategy has issued more than $40 billion in capital in 23 months to finance their Bitcoin purchases and service their existing debt and preferred shares. According to analysts, Strategy’s current software business generates negative cash flow. If this continues and their interest payments / preferred dividends continue to increase, Strategy will be forced to continue to raise to finance those activities. The only issue with this is that Bitcoin’s price has pulled back heavily and has decreased Strategy’s net asset value per share even more. Currently, shares are trading at their lowest EV/NAV in over 18 months (It is a premium that calculates how Strategy’s stock price compares to the value of its Bitcoin holdings per share, minus debt and preferred equity):

The premium that Strategy shares traded at allowed the company to raise more capital. Without it, investors in Strategy are diluted and better off buying Bitcoin directly.

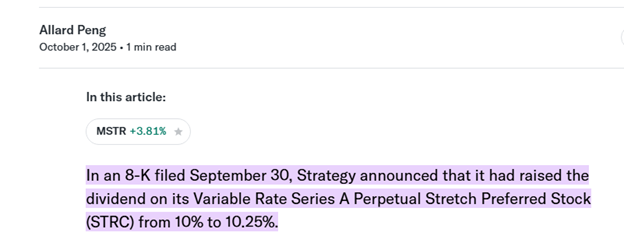

Strategy has also raised its dividends on its preferred shares to attract investors. Essentially, every time their preferred shares have fallen below par, they raise the dividend. If this confidence breaks, Strategy will be forced to sell its Bitcoin, which destroys its investment thesis. Strategy’s forced sales could also greatly impact Bitcoin’s market in the short term, as many argue there is not enough liquidity to absorb a large sale due to margin calls and capitulations. Here is an article from Reuters that explains a recent rise in their dividend from October:

In recent months, Strategy shares have tanked and are near 52-week lows. Shares are down 41% this year and 39% over the last month, while Bitcoin is down only 5% in 2025. Institutions have also been dumping Strategy for a variety of reasons. A major reason has to do with index investing; the MSCI is currently deciding whether firms with more than 50% of their assets in digital assets should be eligible for traditional equity indices. Currently Strategy is nearly 75% Bitcoin. Index exclusion would be mechanical, not discretionary. JPMorgan estimates that there could be $2.8 billion in forced selling from index funds, and total outflows could reach $8.8 billion. This could be 15-20% of the Strategy’s market cap liquidating due to algorithm selling, not fundamentals. This index decision from MSCI is due in mid-January, and the market will deliver its impact in the following weeks to months.

Numerous institutions used Strategy shares in recent years to get Bitcoin exposure; however, that tune is slowly changing as the likes of JPMorgan Chase, BlackRock, and Vanguard have trimmed their Strategy holdings in recent quarters.

This piece is not arguing about Bitcoin and its survival. Bitcoin will outlive Strategy. It is laying out the issues with Strategy’s Bitcoin strategy. For one, this amount of leverage is highly risky, especially when the underlying asset is an extremely volatile asset. Strategy will reportedly face margin calls if the price of Bitcoin dips below $74,430, which would force asset sales or restructuring. Strategy has $270 billion in liabilities outstanding while its market cap is approximately $50 billion.

Strategy more than likely will need to do something to avoid disaster, like restructure or shrink, especially if the MSCI decides not to include companies with more than 50% of their assets in digital assets in traditional equity indices. For the first time in a while, the corporate Bitcoin treasury model has some serious question marks, and many are noticing, including us.

Couche Tard update

Alimentation Couche-Tard, a Canadian-based multinational operator of convenience stores, reported some strong numbers in its 2nd quarter earnings (fiscal 2026) on Monday. If you have been a long-time reader of this commentary, you know that we like the company and have owned it for almost two decades now in some of our longest-standing investor accounts.

Shares jumped almost 5% on Tuesday morning after the strong print, a sign that a trend reversal could be coming. ATD shares are down year-to-date and over the last year due to investor sentiment, weak expectations, and a big M&A overhang from a proposed acquisition for 7-11 (one of ATD’s largest competitors). ATD abandoned this massive acquisition in July after failing to get 7-11’s parent company to seriously engage.

ATD slightly missed quarterly earnings-per-share and revenue estimates; however, both figures grew year-over-year. This is only the second time in two years that ATD has seen its EPS rise YoY. The company reported strong merchandise and service revenue as well as same-store sales across all its markets during the quarter. The biggest positive signal from the company’s earnings report was share buybacks; ATD repurchased $900 million (U.S.) in shares during the quarter, reflecting management’s opinion on the current value of ATD shares. ATD currently has a buyback program that allows for the repurchase of 10% of the outstanding public float.

The company also announced an increase in its dividend of 10.21%.

The results paint a positive picture for ATD, as this is the second straight quarter the company has reported positive and improving key performance indicators.

ATD CEO Alex Miller said the firm continues to look at a few options for acquisitions, stating that the firm is active in Canada, the U.S., and Europe. Miller went on to say that they continue to engage firms and are seeing a lot of deal flow in the industry. For those of you who do not know, the convenience store industry across the world and in the U.S. is quite fragmented, giving ATD ample room for growth and opportunity. According to industry data from 2023, 60% of convenience stores had single-store owners in the U.S.

We think this return to discipline and conservative acquisition approach by management will continue to deliver growth and value to ATD shares and shareholders (like us). Abandoning the 7-11 deal but still engaging in M&A is a positive sign in our eyes. A 7-11 deal would be massive and would result in ATD adding a large amount of leverage and would have diluted ATD shareholders by approximately 50% according to some analysts. We think the deal was high risk, high reward. Historically, ATD has grown through small and regional acquisitions that marginally increased the company’s exposure. The 7-11 deal would have been a different animal; it would have been transformational but highly risky. The abandonment of this deal gets ATD back on track to steady and consistent growth, a compounder that we continue to believe in.

Management also stated the company will continue to integrate recent acquisitions, including GetGo, with early synergies to help drive growth. They also pointed to loyalty programs and digital enhancements as two initiatives that the company hopes will boost customer spending and frequency on items such as food and beverages. ATD also announced a goal to add 500 new locations by 2028. This year, the company aims to open 100 new locations, with 73 currently under construction. In order to support this growth, ATD has opened a 266,000 square foot distribution center in Minnesota, which will supply 500 locations in the upper Midwest. Two more large distribution centers will open soon in Missouri and Ohio that will further support growth and enhance supply chain efficiency for the convenience store giant. This deal will be funded through cash flows and a recent debt issuance of senior unsecured notes.

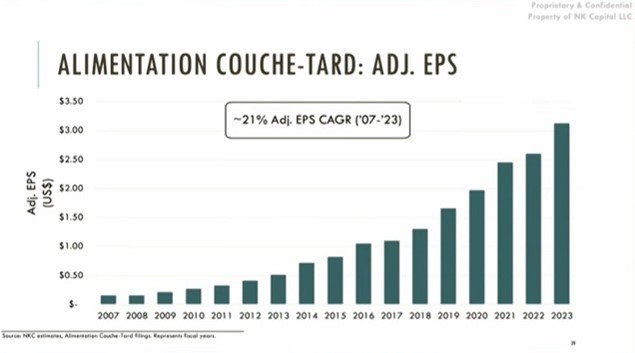

From 2007 to 2023, ATD increased its adjusted EPS by 21% annually, according to NK Capital LLC:

That is a trend we like to follow and one we believe will resume moving forward.

We expect adjusted and non-adjusted EPS to expand over the next 3 years, as well as free cash flow.

We also believe ATD remains undervalued; it is currently trading at 17x forward earnings and 9x EV/EBITDA, in line / slightly cheap versus various competitors (Seven & I Holdings, Casey’s General Stores, Dollarama, George Weston). ATD is more expensive than Seven & I Holdings and its grocery stores, but cheaper than other competitors like Dollarama and Casey’s General Store. ATD’s valuation reflects a company with strong growth prospects that continues to pivot from fuel dominance towards higher-margin in-store offerings. Fuel margins have been facing pressure in recent periods due to EV adoption. With EPS expected to grow around high single digits to low double digits annually, ATD screens are looking forward on an earnings basis than they do on sales, thanks to margin expansion and capital returns. ATD is expected to have stronger EPS growth than all of its competitors, other than Dollarama.

ATD EBITDA is expected to have double-digit growth to 2028, much higher than competitors and ATD’s grocery peers. However, this aggressive plan from ATD involves elevated execution risk, which justifies the slight premium that shares trade at relative to some competitors.

On the risk front, ATD is exposed to transition risk (due to its reliance on fuel sales), inflation risk, execution / operational risk (mentioned above regarding strategy), and valuation risk. We think most of these risk factors are mitigated by various factors, including ATD’s strong history of execution, its experienced and strong management team, ATD’s supply chain expansion, and ATD’s clean energy initiative. ATD continues to actively advance its clean energy strategy with a strong focus on expanding EV charging infrastructure. The company operates 2,400 charging points globally and plans to install 200 new charging stations across North America over the next few years. The company has also focused on diversifying its revenue through nonfuel channels in recent years, including in-store merchandise and car washes.

Overall, we remain bullish about our long-term holding of ATD and believe this week’s earnings call reaffirms our long-term view on ATD. Although share performance has lagged over the last year, we think now could be an inflection point where ATD shares will have a lot of interest due to their sheer value.

Disclaimer: MacNicol & Associates Asset Management holds shares of Alimentation Couche-Tard Inc. across various client accounts.

Analog devices reports

Analog Devices (ADI), an American semiconductor company specializing in data conversion, signal processing, and power management technology headquartered in Massachusetts, reported its fourth-quarter earnings on Wednesday. Earnings beat estimates, and sales grew once again year-over-year, sending shares to all-time highs.

We briefly bring this up as we added some exposure to select client accounts over the last few months. We did this because we see ADI as a value AI play where we have seen and still see more upside and growth. The company, from a fundamental standpoint, is outright inexpensive, trading at 25 times forward earnings with a strong growth rate. You cannot buy companies at that multiple in some defensive industries.

Next week, we will dive deeper into the company’s earnings, but I briefly wanted to mention the strong beat before the holiday weekend.

Disclaimer: MacNicol & Associates Asset Management holds shares of Analog Devices (ADI: NYSE) in select client accounts.

MacNicol & Associates Asset Management

November 28th, 2025

Download in PDF format:

The Weekly Beacon November 28 2025 US

{kind=link}

{kind=link}